Green energy solutions for climate change in the Asia-Pacific

Energy drives everything. In today’s societies oil, gas and coal are the standard sources for the energy we need to live, work, move around and consume. But this is changing, and the shift is both necessary and urgent. Our reliance on fossil fuels must come to an end, or at least be severely limited, if we are to have a chance of avoiding the worst climatic changes and impacts. This critical need was acknowledged on the global stage at the 28th Conference of Parties (COP28) of the United Nations Framework Convention on Climate Change (UNFCCC) in 2023, which closed with an agreement officially marking the beginning of the end to fossil fuels and paving the way for a rapid energy transition. This ambition must be sustained.

The team behind the Green Technology books is admittedly somewhat techno-optimistic, and we do see progress even though it is too slow. The pace of deployment of new technologies is not on par with the gravity of the climate change challenges, but there is progress and not least a plethora of innovation and new technology which is already available and feasible. The Green Technology Books, and the WIPO GREEN Database of Needs and Green Technologies to which they link, are our modest contributions to help speed up the deployment of much-needed solutions. By showing what is available, and what is coming very soon, we hope to bridge the perceived knowledge gap between needs and solutions. The WIPO GREEN database is an active matchmaking tool and through the link to the database, the Green Technology Books also become active matchmaking tools. Both are free UN resources, and we strongly encourage you to explore what they have to offer.

The pace of deployment of new technologies is not on par with the gravity of the climate change challenges

The Green Technology Book has, since its inauguration in late 2022, been published in three editions. In the first, we presented the technologies available for climate adaptation, an area which we found did not receive enough attention. We closely examined technologies for agriculture, cities and water, including coastal protection. The second edition focused on climate change mitigation technologies, as well as agriculture and cities, but also the hard to abate industries steel and cement. The third edition focused specifically on energy technologies for climate change with chapters addressing urban areas, rural communities including agriculture, and the service areas of water, supermarkets and data centers. Common to all the Green Technology Books is a simple and accessible style and short, concise sections describing various technology developments and trends in the focus areas, followed by a listing of technology examples. We divide these into three groups: proven technologies, which have been on the market for some time and hence are well established; frontier technologies that are available but relatively new; and horizon technologies, which are expected to become available soon. We have designed the books to help anyone curious about the potential of technology easily find the areas and solutions most relevant to them. In the digital version, it only takes a click to go to the WIPO GREEN database and find more details and a link to the solution provider. We would be grateful if you could let us know (email: info@wipogreen.wipo.int) whether you find what you are looking for or share how you are using our work.

The World Intellectual Property Organization (WIPO) is a UN specialized agency, established in 1967 with the mandate to promote invention and creativity for the economic, social and cultural development of all countries through a balanced and effective international intellectual property (IP) system. In WIPO GREEN and the Green Technology Books, we focus on showing how innovation and technology are part of the solutions to climate change, food security and the environment. By doing so we support the national systems of Innovation (NSI) and technology transfer, both of which are based on and enabled by the international IP system.

This edition of the Green Technology Book was created as a special EXPO25 edition of the Energy Solutions for Climate Change edition. It builds on many of the same technology areas but applies a specific Asia-Pacific focus. The 2025 World Exposition (EXPO25) Designing Future Society for Our Lives takes place in Osaka, Japan

The Asia-Pacific climate change focus

The Asia-Pacific region is remarkable for many reasons, one being the spectacular economic growth in several countries. It is a region with stark contrasts and is home to both some of the richest and poorest countries in the world. Additionally, it boasts high population growth in some countries and is home to the world’s most populous nations. High economic growth coupled with large and growing populations also mean an increasing demand for energy. Changed demographic strata, notably emerging large middle-classes with new food and living style preferences, increase pressure on natural resources and the demand for energy to support new home appliances and transport needs. But it is also a region which is home to some of the most innovation-capable countries in the world, with Singapore, the Republic of Korea, China and Japan in the top 13 countries in that order in the 2024 WIPO Global Innovation Index

Asia-Pacific is a region which is home to some of the most innovation-capable countries in the world

Reflecting the trends in the region as well as some of the sectors where the potential for green technology transformation is high, we have chosen to focus this edition on urban households, public spaces, transport and water utilities, in rural areas on households and communities, fisheries and aquaculture, agriculture on-farm and post-harvest, and hotels and shopping malls as service areas. For more details on how we create the book, select technologies etc., please refer to the methodology section.

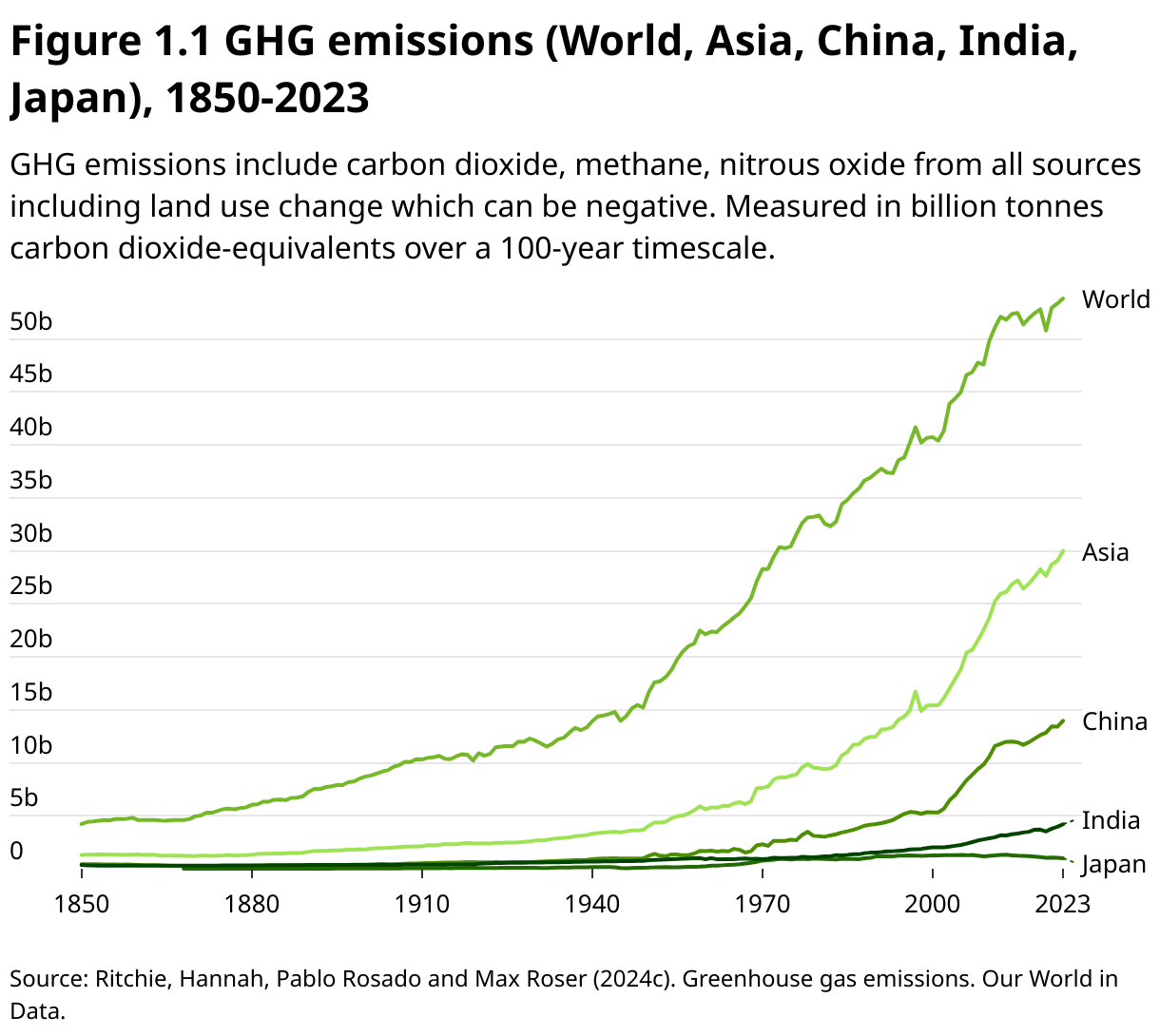

Fossil fuels still dominate the energy and GHG emissions landscape of the Asia-Pacific region

The region consumes approximately 46% of the world’s energy

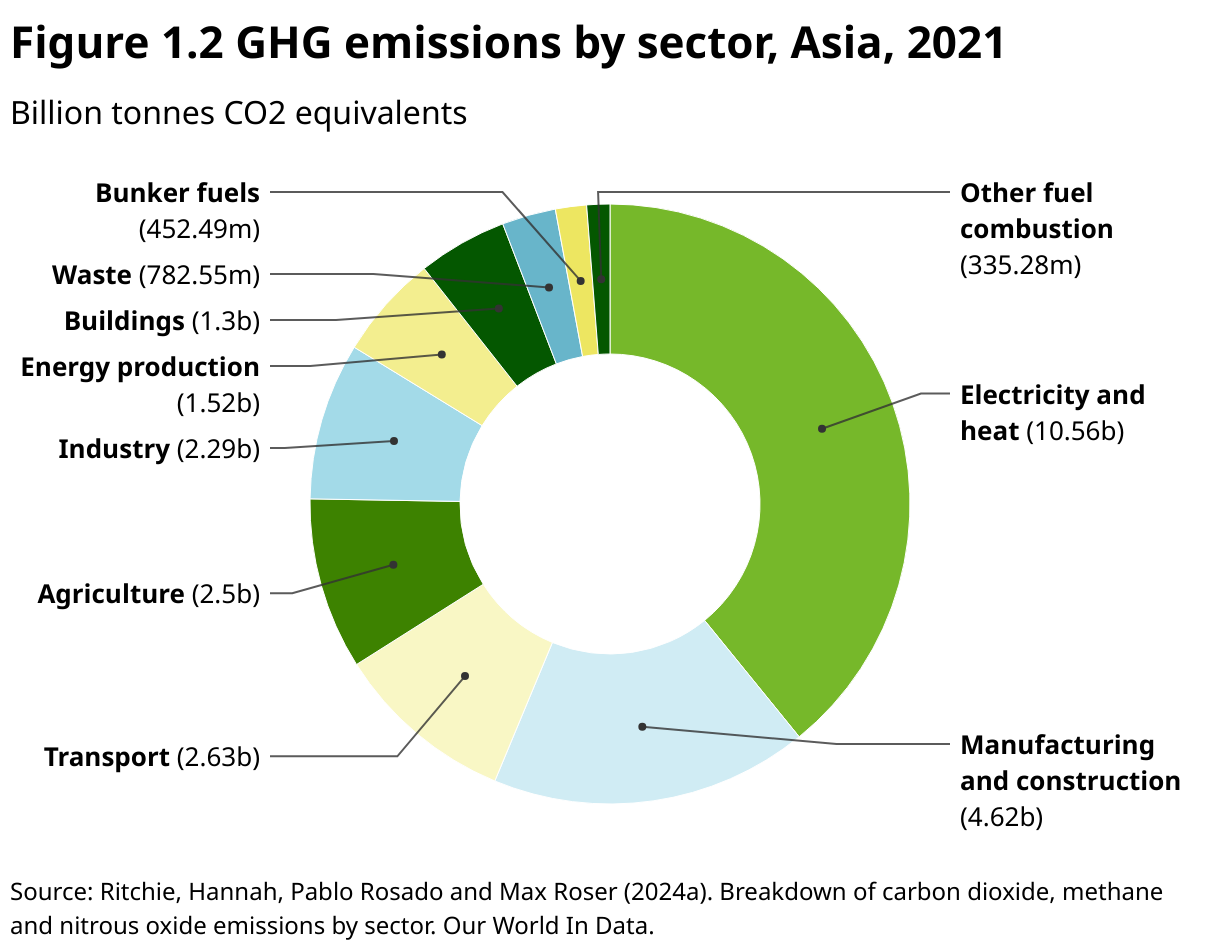

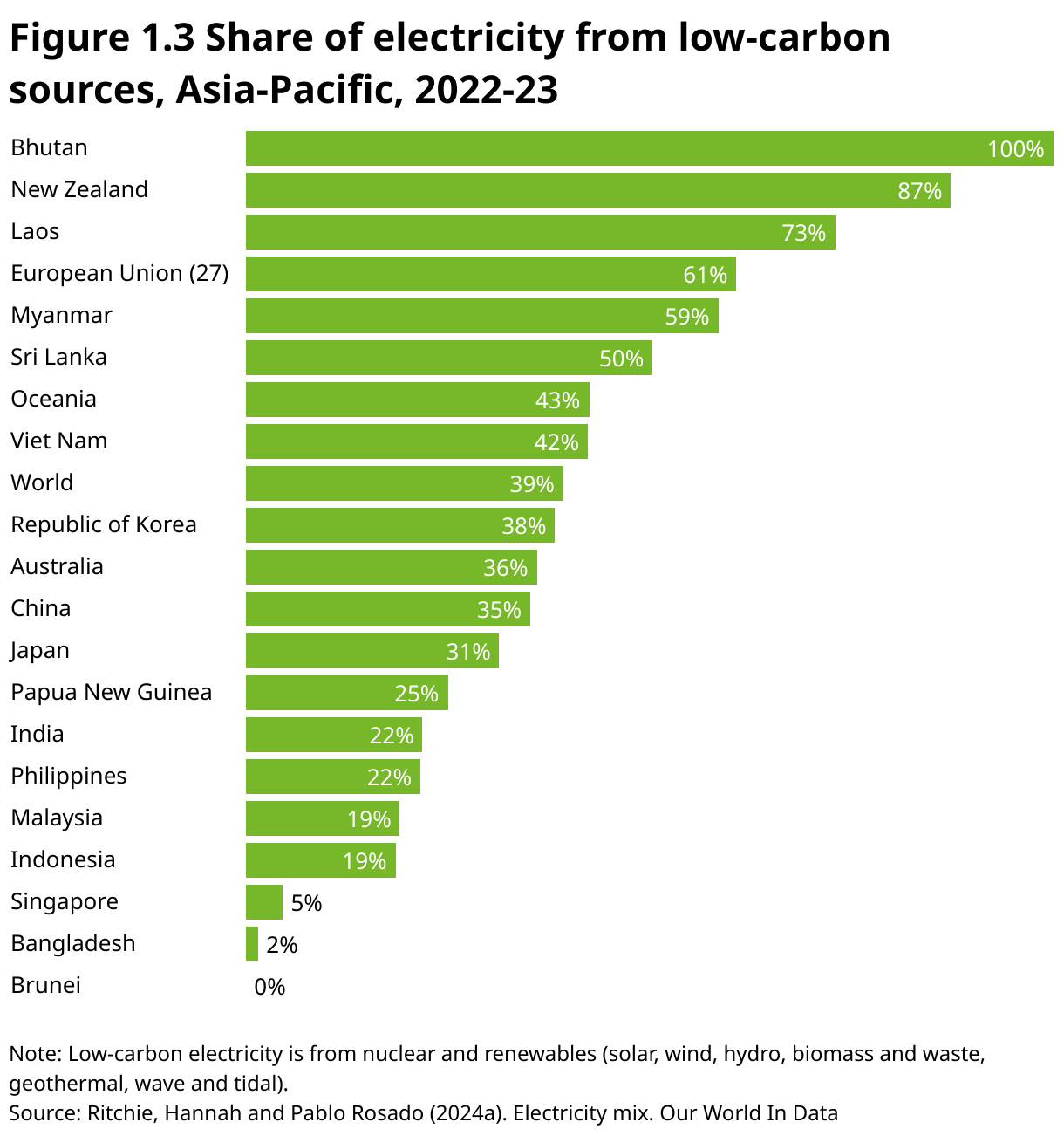

As the region is highly diverse, rural connectivity to national electricity grids also varies considerably. The electricity grid is key for many of the low-carbon solutions that are being implemented, simply because they are electricity driven with many requiring frequent recharging. This means that they are not greener than the electricity that feeds them. The region benefits from a significant hydropower potential in many countries which contributes to greening the energy mix in the electricity grid. Major investments in other renewable energy sources, especially solar PV and wind, are resulting in a positive trend toward greener grids, not least spearheaded by the very large and rapid solar PV investments in China. Figure 1.3 illustrates the large regional diversity in low-carbon energy (renewable and nuclear) in the electricity mix. It ranges from countries with almost no low-carbon energy in the mix to extreme cases like Bhutan, New Zealand and the Lao PDR with massive hydropower resources.

Technology available for a region vulnerable to climate change

The region is highly vulnerable to climate change impacts. This stems from a combination of factors: several poor countries with limited resilience capacity, large populations or even whole countries that are prone to flooding and other extreme events, and climate systems which are vulnerable to disturbances from climate change such as the yearly monsoon pattern. This implies that climate change adaptation is crucial, and for some countries by far the most important factor. This edition of the Green Technology Book focuses on energy technologies that are often associated with climate change mitigation. However, as was also observed in the adaptation and mitigation editions of the Green Technology Book and is pointed out repeatedly in the following chapters, many solutions have dual advantages in that they may help bring down GHG emissions while also reducing vulnerability and increasing resilience – in short, supporting climate change adaptation.

The region benefits from a significant hydropower potential in many countries which contributes to greening the energy mix in the electricity grid

The Sharm El Sheikh Adaptation Agenda, introduced at COP27, established a target for energy plans to include climate adaptation perspectives for energy generation, transmission and distribution infrastructure at national and sub-national levels. Here, the focus is often on enabling decentralized energy systems through extended battery storage capacity and transmission and distribution networks. The targets also consider how transport infrastructure can become resilient to climate hazards through the adoption of new technology, design and materials. While these technologies are not specified, and there is a global lack of standards on the topic, the Green Technology Book adaptation edition presents a number of adaptation solutions.

With regard to the incorporation of energy resilience into national adaptation planning, the International Energy Agency (IEA) has found that even where countries have national strategies or adaptation plans, pressing needs for climate resilience in the electricity sector have not been addressed, evidenced by the fact that more than half of the 31 IEA member countries have limited or no information on the climate resilience of electricity systems

Understanding the link between energy access and climate adaptation is crucial, and yet this is often overlooked. Energy services themselves, such as cooling and back-up energy and water supply, are essential to respond to climate change impacts including drought, temperature rise and natural disasters

Agriculture and renewable energy production can successfully coexist using agrivoltaics. Maximizing land and water use via agrivoltaics and aquavoltaics (energy technologies that allow for simultaneous agricultural or aquacultural use alongside energy production) achieves synergies between mitigation and adaptation for rural communities, boosting both renewable energy supply and food production. This co-location provides solutions for land constraints, which will be increasingly important as the population grows and productive land becomes scarcer.

Micro-grids are increasingly useful to populations impacted by natural disasters such as bush fires, storms and flooding whose frequency and severity have been exacerbated by climate change. Conventional micro-grids relying on diesel generators contribute to GHG emissions and are costly. Local smaller-scale renewable energy sources can deliver more reliable services while mitigating climate change.

Energy efficiency measures are often an underutilized opportunity. The ambitions for build-back-better following the COVID-19 pandemic looks increasingly like a missed opportunity as we return to pre-pandemic habits and procedures. The current (mid-2025) tense geo-political situation, along with many countries being forced to allocate larger budgets for defense, risks derailing and delaying climate action otherwise well underway. However, climate change will not go away, even if we are preoccupied with other priorities, and any delay will only worsen its consequences. That is why we talk of delay. Climate change can only be ignored in the short term and the impacts will continue to become worse as CO2 content in the atmosphere increases, and global temperatures and sea levels rise.

Technology transfer in all directions

The international and national systems of innovation are highly efficient in producing new solutions. Innovation is still predominantly originating in the more developed and affluent countries as innovation can be expensive and often requires highly specialized skills as well as other factors important for an efficient innovation ecosystem. For a more thorough understanding of this, we encourage you to visit the WIPO Global Innovation Index and discover the many factors included in the innovation ecosystem assessments.

But innovation is also taking place in much less developed and affluent countries. It may not always be as high-tech or advanced as other solutions, but it may be exactly what is needed in a specific context. It is one of the ambitions of the team behind the Green Technology Books to bring this innovation to the forefront. We believe that there is huge potential for South–South technology transfer where many solutions may be more easily adaptable to the local situation. Innovation is also a matter of being able to adapt solutions originating elsewhere to local conditions, and this factor may be hugely important. It looks like technology adaptive capacity is often overlooked or underappreciated. It can be challenging to find such technologies as often they are not as visible, market-oriented or competitive as technologies from developed countries which often are emerging in a highly competitive space. We do our best to uncover local solutions, but we know we are only seeing a fraction of what is taking place. Finally, it should be noted that South–North technology transfer is something we should expect to see more of in the coming years. We hope that by showing the solutions that are available or rapidly becoming available, also from developing countries, we can help contribute to speeding up this process. We need all available solutions, and we need to implement them fast. This is, in a nutshell, what we hope to help achieve.

Innovation is taking place in less developed and affluent countries. It may not always be as high-tech or advanced, but it may be exactly what is needed

Make climate change good business through innovation

Maybe the political will to fight climate change is waning among some, but this does not stop developments in innovation and technology developments which are increasingly making climate change solutions good business. Already solar and wind are energy sources competitive with fossil fuel, meaning that it simply makes sense economically to go green. The best guarantee for rapid green transition is to make it good business, also for the individual company, farmer and household. There is no need for short-lived government sponsored support programs if a solution is good for the bottom line. It may take support initiatives in various forms to reach that point, but this is not new and holds true for many new solutions, be that in climate change or not. Do not expect that a company or a farmer with narrow margins will transition to green technology just to reduce emissions. Even if they want to, they may not be able to afford the risk associated with change. But if a solution is reducing emissions and/or increasing resilience while also increasing earnings, then climate change ambitions and economic considerations are pulling in the same direction. This is what we must achieve, and this is what we are looking for. In the Green Technology Books we of course cannot guarantee that the solutions we show as examples are economically beneficial, as this will always depend on the individual context. But we can show what is there and is available and it is then up to the reader to explore whether it is also economically feasible. There is increasingly a good chance that it will be.

Climate finance and corporation in the Asia-Pacific region

Unlocking climate funds for inclusive clean energy growth

Climate finance refers to local, national or international funding, sourced from public, private or alternative channels, that is used to support climate change mitigation and adaptation efforts. It can be mobilized through mechanisms under the UNFCCC or through bilateral and multilateral institutions. Climate funds continue to play a critical role in supporting renewable energy and energy efficiency projects across the Asia-Pacific region.

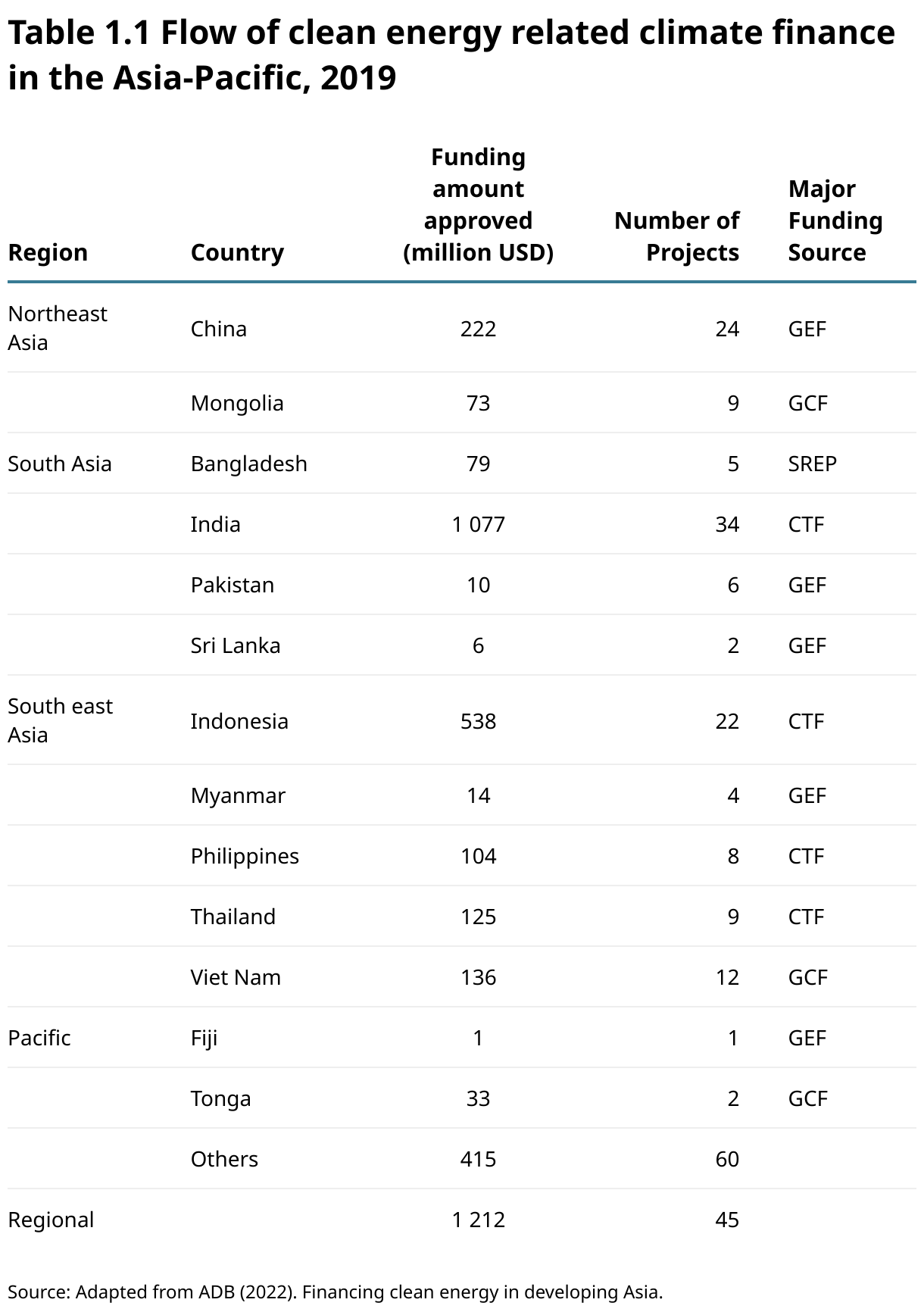

The Climate Investment Funds (CIF) serve as an umbrella mechanism to promote low-carbon and climate-resilient development in developing countries. As of 2019, the Clean Technology Fund (CTF), Green Climate Fund (GCF), and Global Environment Facility (GEF) were the largest multilateral climate funds by total investment volume, providing significant financing to countries in the region (see Table 1.1). The GCF supports clean energy and energy access initiatives, while the GEF focuses more on climate adaptation and sustainable development. The GEF had the broadest reach, with 168 active projects as of February 2019, while programs like the Scaling Up Renewable Energy Program (SREP) focus on fewer, larger-scale infrastructure investments. Between 2003 and 2017, just three countries, China, India and Indonesia, accounted for 53% of the climate finance received in the region, reflecting the scale and maturity of their economies and energy markets

Recent data indicate a strong post-COVID-19 surge in global investment in energy transition technologies. In 2022, global investments in these technologies reached USD 1.3 trillion, an increase of nearly 70% from pre-pandemic levels in 2019. Asia has emerged as a key destination for this capital, with East and South Asia alone receiving over three-quarters of global investments in renewable energy technologies. This trend reinforces the region’s growing importance in the global clean energy transition

Several other global programs with dedicated clean energy mandates are active across Asia, such as the Global Climate Partnership Fund. These funds are well-positioned to support project preparation and mobilize investment.

However, although climate funds are well established in the region, many focus on large-scale projects and often face challenges in developing pipelines for smaller, decentralized initiatives due to high transaction costs. This poses a barrier for smaller economies, especially in the Pacific and parts of Central Asia, where energy markets remain relatively underdeveloped. To bridge this gap, there is a strong need for investment facilitation mechanisms that help viable smaller projects, also in the private sector, meet funding criteria. Enhancing access to these funds could significantly accelerate clean energy deployment in the region

Multilateral development banks driving and de-risking investment in Asia’s energy finance landscape

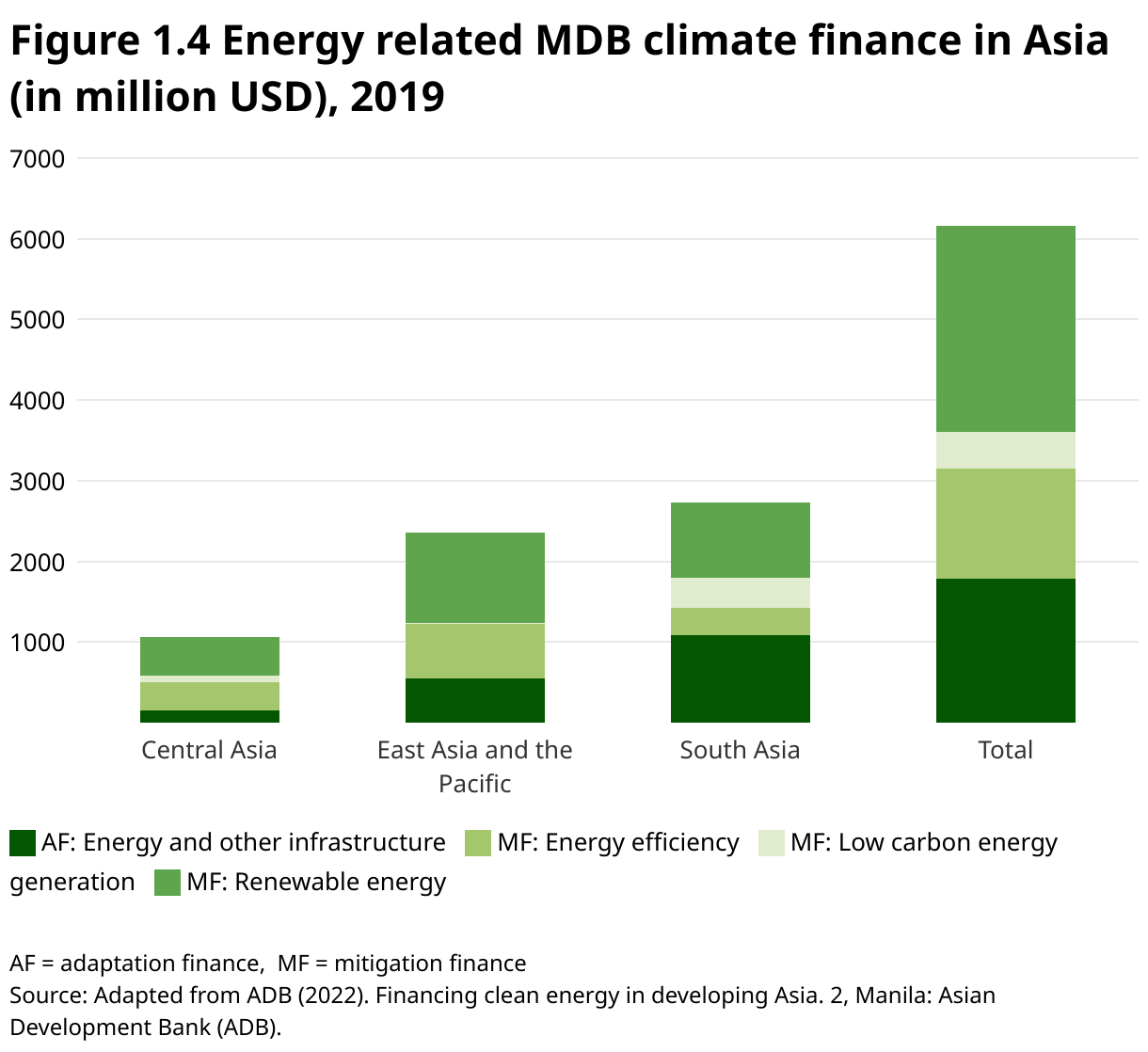

Multilateral Development Banks (MDBs) have been pivotal in advancing clean energy across Asia, particularly in the early phases of renewable energy deployment. Initially, development finance institutions (DFIs) led investments in the region, supporting capacity building, technology transfer, feasibility studies and technical cooperation. As utility-scale solar and wind projects became more bankable, private sector participation increased markedly after 2010, with MDBs continuing to play a complementary role by de-risking investments and strengthening enabling environments. This is reflected in the scale and focus of MDB climate finance flows to the region. As seen in figure 1.4, in 2019 alone, the region received over USD 6 billion in MDB funding, 44% of which went to South Asia and 38% to East Asia. Approximately 53% of this financing was allocated to renewable energy and 31% to energy efficiency initiatives

The World Bank and the Asian Development Bank (ADB) are the primary MDBs supporting clean energy investments in the region. The European Bank for Reconstruction and Development (EBRD) is also active, particularly in Central Asia. New MDBs such as the Asian Infrastructure Investment Bank (AIIB) and the New Development Bank (NDB), established in 2016, have increasingly contributed to clean energy and sustainable transport. By the end of 2019, the NDB had committed USD 3.5 billion to clean energy initiatives

Between 2009 and 2016, Southeast Asia attracted about USD 6 billion in development bank investments, largely in the form of loans (73%), concessional loans (10%) and equity (3%). The World Bank, ADB and Japan Bank for International Cooperation (JBIC) were the largest contributors. Hydropower has been a focus of many MDBs, especially in South and Southeast Asia, while AIIB has emphasized large-scale renewable projects

Private sector offers promising opportunities for clean energy investment in Asia and the Pacific

Private financing originates from individual and corporate sources and is channelled into investments through a range of financial intermediaries. Since 2010, there has been a noticeable shift toward private financing for utility-scale clean energy projects across the region. East Asia and the Pacific have led this trend, mobilizing around USD 100 billion annually, while South Asia has attracted approximately one-tenth of that amount. Most of this investment has remained domestic, with about 90% directed toward solar and wind technologies, reflecting their technological maturity and bankability

In earlier stages, venture capital played a key role in advancing renewable technologies. In 2019, venture capital and private equity invested USD 3 billion in renewable energy, with 60% allocated to solar PV. India emerged as the largest recipient, securing USD 1.4 billion

However, as solar and wind technologies have matured and now dominate the renewable energy market, funding dynamics have shifted, with many companies increasingly conducting research and development internally. In contrast, emerging clean energy solutions such as freshwater and near-shore floating solar PV still require substantial support from venture capital and private equity. Ocean-based technologies, including marine and tidal energy, are gaining attention, yet face similar challenges. Likewise, progress in biofuels, including production of green hydrogen and marine energy, has been less than anticipated. As a result, investment in these areas remains limited, underscoring the need for targeted venture capital and innovation-focused financing to help bring these next-generation technologies to scale

Private sector banks and financiers also represent major potential sources of funding, often investing directly in businesses across developing countries. However, emerging low-carbon technologies face higher financing hurdles due to uncertainties in performance, supply chains and profitability. To support their development, governments and development finance institutions can offer risk-sharing mechanisms, concessional finance and guarantees

A new trend is emerging, where a pool of capital from foundations is being used for specific purposes. For example, four United States of America (US)-based foundations – the William and Flora Hewlett, John D. and Catherine T. MacArthur, and David and Lucile Packard Foundations, and Jeremy and Hannelore Grantham Environmental Trust – have jointly supported multiple initiatives in India, including the US–India Catalytic Solar Finance Program, to support development of risk mitigation vehicles for the renewable energy sector. This trend extends to a global pool of institutional or private funds, who are willing and prepared to support India’s renewable energy transformation over the next decade.

(Excerpt from

Renewable energy dominates climate finance in the Asia-Pacific region

In 2022, 302 cities across Asia-Pacific reported through the CDP-ICLEI

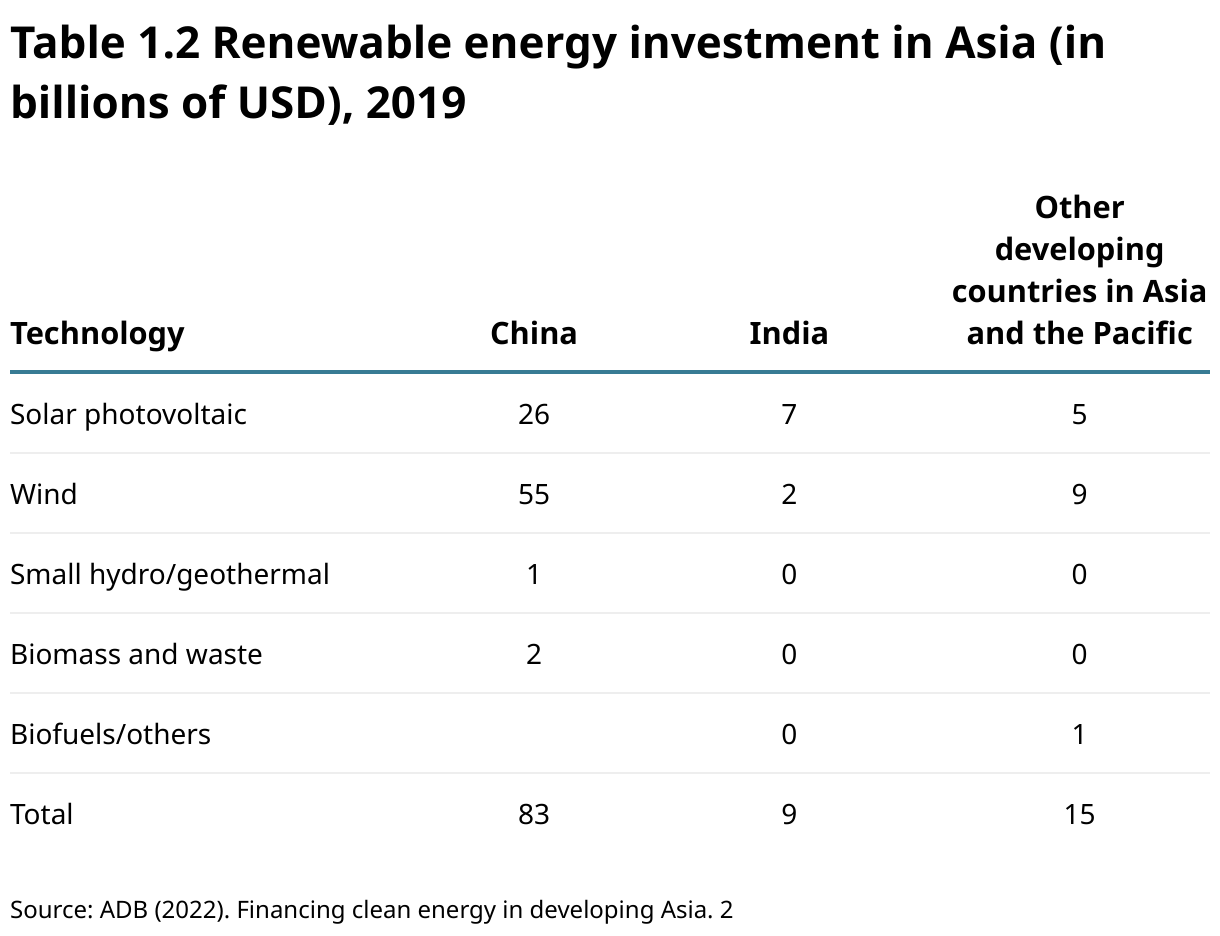

Investment in renewable energy has been increasing at a rate of 34% in the Asia-Pacific region since 2004, although much of it is in China and India

In Southeast Asia, solar PV and solar thermal are gaining investor interest, but investment patterns vary across the region based on resource availability, demographics and national priorities. For example, in countries with abundant hydroelectric resources, like Cambodia and the Lao People’s Democratic Republic, international funds have primarily supported hydropower development. Indonesia, by contrast, has focused heavily on geothermal energy, far outpacing investments in solar and wind power.

Despite growing interest, access to finance for large-scale renewable energy projects remains a key challenge in Southeast Asia. Barriers include permission and ownership restrictions, grid limitations and underdeveloped financial institutions in lower-income countries. While some local and development banks are engaged, many domestic banks lack the expertise or investment-ready projects to participate fully. Strengthening institutional capacity and creating more bankable projects are essential for scaling up investments

Overall, cities are prioritizing mitigation over adaptation, despite rising climate risks. As explained in the introduction section of this chapter, many energy technologies have both mitigation and adaptation qualities. Between 2018 and 2019, mitigation finance, especially in the energy sector, dominated climate funding in the Asia-Pacific region, totaling USD 472.5 billion, or 91% of the total flow

Pacific Island states face challenges accessing both technology and financing for the energy transition

Achieving energy security remains a major challenge for Pacific Island states due to their geographic isolation, relatively small economies and reliance on costly imported fuel. While renewable energy offers a promising alternative, many islands are exposed to cyclones, corrosive marine environments and difficult logistics, making infrastructure deployment costly and technically complex.

Despite the constraints, the Pacific region is seeing growing interest in small-scale renewable energy solutions, especially off-grid and micro/mini-grid solar systems

Despite the constraints, the Pacific region is seeing growing interest in small-scale renewable energy solutions, especially off-grid and micro/mini-grid solar systems

However, financing remains one of the biggest hurdles in transitioning to clean energy in the Pacific. Shifting from centralized diesel systems to solar, wind or hydroelectric plants involves significant capital investment, which many countries in the region cannot afford on their own. In addition, private sector investment in renewable energy in the Pacific is quite modest

ADB is a major funder of renewable projects in the region, including through the Pacific Renewable Energy Program (PREP), a financing structure that is designed to finance a series of renewable energy projects in the small Pacific Island states. ADB has also supported the long-standing Promoting Energy Efficiency in the Pacific initiative, which has helped catalyze energy efficiency investments across the region. Improving energy efficiency can also ease the cost of fuel imports and help existing power systems meet demand more affordably and thereby may result in reduced investment needed for the expansion of electricity generation (ADB, 2021).

International climate finance and technology cooperation must go hand in hand

At COP28, countries committed to tripling renewable energy capacity and doubling energy efficiency improvements –an ambition that places energy efficiency at the heart of global and regional energy policymaking

Most financial resources are held by developed countries, making it hard for many Asian nations to attract the large investments needed for big changes

The region holds a window of opportunity to leapfrog into cleaner, more sustainable systems. Yet progress is often hindered by structural barriers, including high upfront costs of clean technologies, limited access to affordable finance and dependence on imported technologies

A key challenge lies in the global imbalance in financial and technological resources. Most financial resources are held by developed countries, making it hard for many Asian nations to attract the large investments needed for big changes. Moreover, most climate technologies are developed by and exported from developed countries, with China being a notable exception

Strengthening international and regional cooperation is therefore essential. Enhanced South–South and triangular cooperation, including between more technologically advanced Asian countries and their neighbors, can play a significant role in bridging gaps in capacity and access. Initiatives like the India–EU Clean Energy and Climate Partnership, and regional platforms under the Clean Energy Ministerial involving Asian countries such as China, India, Indonesia and Japan, offer valuable pathways for knowledge exchange and collaborative innovation.

The role of innovation and intellectual property rights for clean energy technologies

Innovation for a sustainable future: Asia’s commitment to the Sustainable Development Goals

Globally, innovation linked to the Sustainable Development Goals (SDGs) has seen steady growth, with SDG 7 (Affordable and Clean Energy) and SDG 13 (Climate Action) showing particularly strong upward trends compared to most other SDGs. This is driven by technological advances in RE and efforts to cut greenhouse gas emissions. It reflects a growing awareness of and consumer preference for cleaner alternatives, aimed at improving energy efficiency and reducing carbon emissions (figure 1.5). Patent applications can be a good proxy for relative innovation activity levels in various sectors. Analyses of patenting patterns show that some technologies contribute to multiple SDGs; for instance, “Greenhouse Gas Emission Reduction” falls under both SDG 9 (Industry, Innovation and Infrastructure) and SDG 13 (Climate Action). While SDG 13 focuses on technologies directly aimed at reducing emissions, SDG 9 includes broader innovations like upgrading infrastructure and retrofitting industries to improve energy efficiency and sustainability

The Asia-Pacific region mirrors this trend, with a sharp rise in clean energy patenting activity reflecting strong alignment with these two SDGs. In China, the innovation landscape is led by companies like CATL, a major innovator and producer of batteries, who owns the second-largest share of SDG-related patents among the top 25 patenting companies in China, underscoring the active innovation in advancing storage technologies essential to clean energy deployment. Japan also demonstrates significant patent contributions toward the SDGs, especially from its top corporate innovators. Toyota Motor has shown a consistent upward trend in SDG-related patent activity, surpassing Panasonic in 2013 to become the country’s leading filer. These patent trends highlight the strategic focus of Japanese industry on low-emission mobility, hydrogen technologies and energy-efficient manufacturing

Patent applications can be a good proxy for relative innovation activity levels in various sectors

In the Republic of Korea, Samsung, the country’s largest patent holder, maintains a vast SDG-related portfolio, accounting for about 25% of its total patents. However, this share has remained stable as the company’s overall patent activity grows across multiple sectors. Other Korean firms, including Hyundai Motor, LG Chemical, LG Electronics and Kia, have shown more varied but generally positive growth trends, particularly in sectors tied to electric vehicles, battery storage and energy-efficient electronics. Overall, the Korean landscape appears more diverse, presenting a mix of company sizes, SDG patent shares and growth trajectories, that range from highly positive to highly negative. This diversity likely stems from market consolidation within the Republic of Korea, where a few major players hold the majority of patents

Although energy patent trends may not directly reflect market demand or predict the commercial success of a technology, analyzing them offers valuable insights into technological advancements, industry trends and regional innovation hubs. For further discussion on the innovation ecosystem for climate change technologies and intellectual property systems, refer to Chapter 2 of the Green Technology Book adaptation edition as well as WIPO patent landscape reports and the WIPO Global Innovation Index. More details on intellectual property rights are highlighted in Box 1.2.

Renewable energy (RE) boom in the Asia-Pacific region

Technological advancements are playing a pivotal role in accelerating the adoption of clean energy across the Asia-Pacific region. Innovations in energy storage, grid modernization and RE generation technologies are significantly improving the efficiency, reliability and scalability of clean energy systems. The declining costs of solar panels, wind turbines and energy storage technologies have made RE more accessible and economically attractive, prompting substantial public and private sector investment. By 2024, utility-scale solar photovoltaic (PV) systems in the Asia-Pacific region had become the most cost-competitive globally, with RE generation proving approximately 13% cheaper than coal. Alongside leading the world in solar PV and onshore wind deployment, the Asia-Pacific region, led by China, is also set to accelerate the deployment of and further increase innovations in alternative clean energy technologies such as offshore wind, floating solar and green hydrogen

Energy patent trends may not directly reflect market demand or predict the commercial success, analyzing them offers valuable insights into technological advancements, industry trends and regional innovation hubs

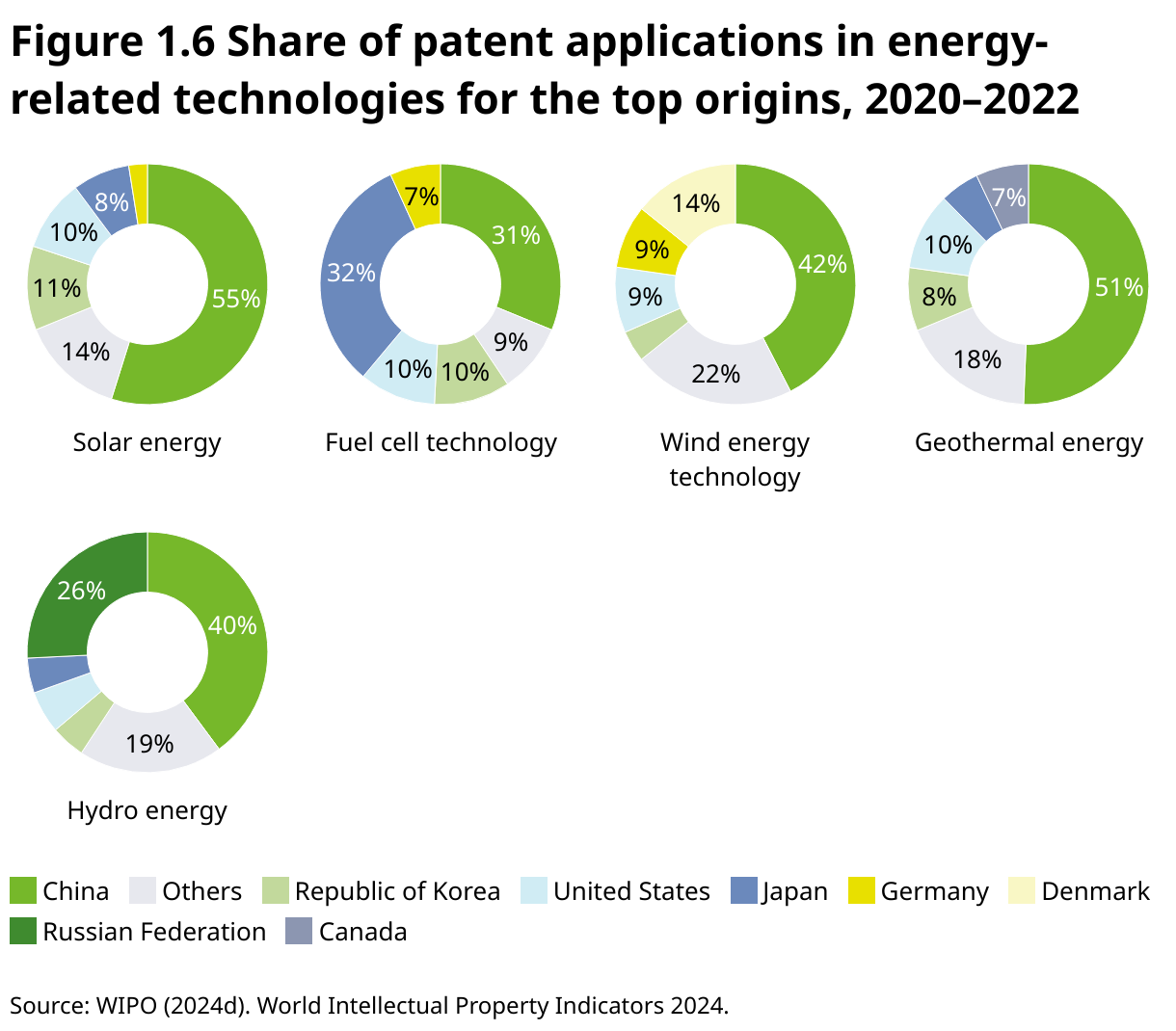

This momentum is mirrored in the region’s innovation landscape and patent activity. From 2007 to 2022, global patent filings for clean energy technologies, covering solar, wind, fuel cells, hydro and geothermal, grew from approximately 29,400 to 44,700 per year. Asia-Pacific countries, particularly China and Japan, have emerged as global leaders in this space. As shown in figure 1.6, China accounted for the highest share of global patent applications in four of the five technologies, including a dominant 54.9% in solar energy and 39.9% in hydro. Meanwhile, Japan led globally in fuel cell innovation, contributing 32.1% of related patents. From 2020 to 2022, solar energy represented more than half of the energy-related patent filings worldwide (54.4%), followed by wind (19.4%), fuel cells (13.2%), hydro (11.4%) and geothermal (1.5%). Here, notable innovation trends include a focus on technologies that enable more cost-effective installation and manufacturing, and new types of organic PV cells design that enable solar integration into windows, wearables and other objects (EPO and IEA, 2021). These trends highlight the Asia-Pacific region’s growing role as a hub of clean energy innovation, with strong potential to shape the global shift toward a more sustainable and low-carbon future

Intellectual property rights (IPR) are central for innovation. International agreements have created the foundations of an IPR system that allows for the protection of innovators’ rights almost worldwide. Multi-territorial protection is crucial for cross-border technology transfer and technology marketing. It is also a cornerstone in the innovation ecosystem as discussed briefly in the introduction section. It is the mandate of WIPO as a UN specialized agency, to ensure that this system is functional and developing, ultimately for the benefit of global development. In relation to technology, patenting is the dominant way to secure IPRs. The system is based on rights granted by national or regional authorities for their respective territories, and there is no such thing as a global patent. While the Patent Cooperation Treaty (PCT) does not provide for centralized patent granting, it does simplify and make more cost effective the process of seeking patents in multiple countries.

A patent provides the innovator with rights to authorize or prevent the use of the invention in a certain territory for a certain period, typically 20 years from filing the application. In exchange, the innovator has to disclose detailed information on the invention publicly available so that anyone can understand, make and further develop an invention when it falls into the public domain. A technology protected by a patent of course cannot be used commercially in a country where a patent is still in force. In countries where no patent was granted, however, such use cannot be prevented by the holder. This significant quality of the IPR system has created an enormous repository of detailed technological information which is made publicly available in several very large patent databases. For example, WIPO’s PATENTSCOPE database contains more than 120 million patent documents. The WIPO GREEN Database of Needs and Green Technologies contains a small selection (>135,000) of green technology patents. A patent contains the description of an invention, but it cannot be known from the patent document whether it is available on the market or even whether it was developed into a solution. WIPO GREEN has therefore created a special search function “Patent2Solution” which uses AI to search for an available solution based on the specific patent document. It can be launched from the patent description in the WIPO GREEN database. Patents can be analyzed for trends and geographical distribution and much more. It is to some degree a measure of innovation and numerous patent studies are published regularly, e.g. the WIPO Patent Landscape Reports, the Global Innovation Index, the World Intellectual Property Indicators and the WIPO Technology Trends Report. Often these analyses are based on patent families which are a group of patents that cover the same invention in different territories and share the same “original” application.

Asia’s dominance in clean transport innovation and market growth

The global transportation sector is undergoing a profound transformation, driven by the rapid rise of electric vehicles (EVs), sustainable fuels and smart mobility solutions. As more EVs hit the roads and alternative fuels such as biodiesel, sustainable aviation fuel and green hydrogen gain traction, fossil fuel dependency is beginning to decline

Across all major transport modalities Asia leads in patent activity, with China, Japan and the Republic of Korea among the global top five countries

Innovation plays a central role in this transition. The global transportation sector has accounted for more than 40% of international patent families (IPFs) in low-carbon energy (LCE) technologies between 2000 and 2019. EV-related patents – including those for fuel cells and charging infrastructure – have surged, overtaking all other road transport technologies by 2011. Additionally, technologies aimed at improving energy efficiency in transport represent nearly one-third of all end-use technology patents, underscoring the sector’s broader push toward sustainability

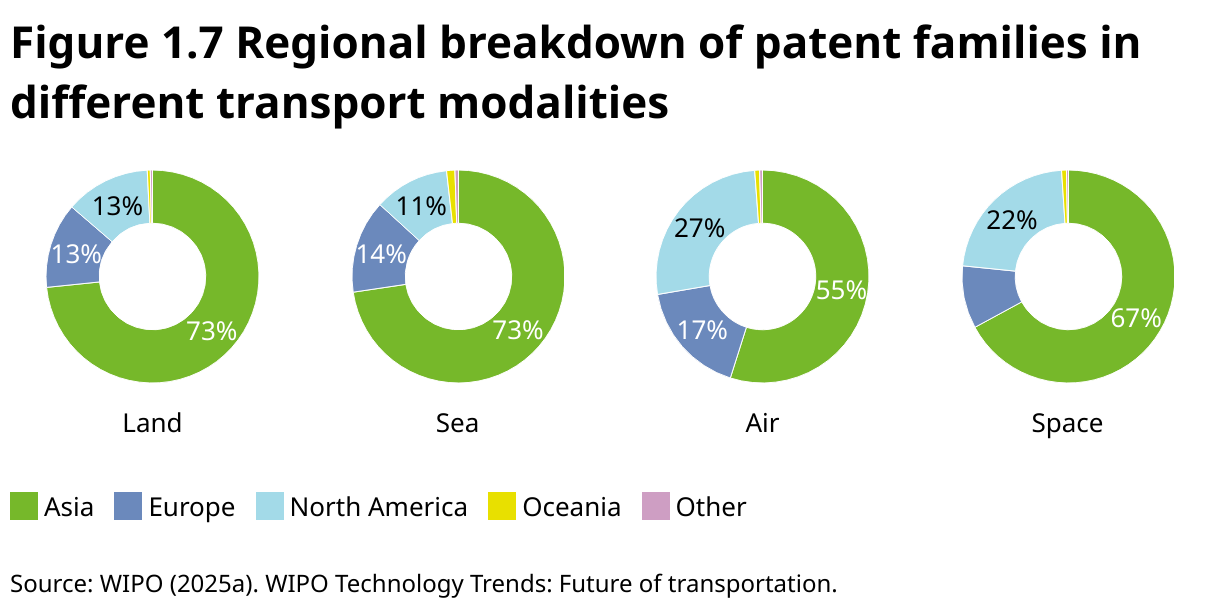

Asia has emerged as the dominant region in transportation innovation. Across all major transport modalities – land, sea, air and rail – Asia leads in patent activity, with China, Japan and the Republic of Korea among the global top five countries (figure 1.7). Since 2018, China has emerged as the primary engine of innovation in this space, with its number of annual patent families nearly doubling from 38,900 to 76,000 by 2023, reflecting a robust 14.3% annual growth rate and underscoring the country’s strategic investment in next-generation transport technologies

While patent data reveals the scale of innovation, market dynamics provide a broader context. The global transportation market is a multi-trillion-dollar industry, with the Asia-Pacific region holding the largest and the fastest-growing share. This growth is propelled by rapid urbanization, population growth and major infrastructure investments, particularly in China and India. Additionally, the sector is being reshaped by the rise of e-commerce, advancements in automation and autonomous vehicles, and shifting regulatory frameworks aimed at sustainability and efficiency

China and Japan dominate global patenting activity in sustainable propulsion, particularly in battery and electric drive technologies

A key sub-sector within this broader transformation is smart transportation, which integrates advanced technologies to improve mobility efficiency, safety and sustainability. Valued at USD 33.4 billion in 2024, the global smart transportation market is expected to reach USD 46.4 billion by 2029, growing at a compounded annual growth rate (CAGR) of 6.8%. Though it currently represents just 0.5% of the overall transportation industry, its role is expanding rapidly. Asia-Pacific is projected to experience the fastest growth, fueled by increasing traffic demands, governmental efforts to reduce greenhouse gas emissions and the emergence of megacities. Key enablers of this growth include technologies such as the internet of things (IoT) and artificial intelligence (AI), which are instrumental in advancing autonomous vehicles, intelligent traffic management systems and integrated mobility platforms. Recent developments highlight growing global collaboration in building smart infrastructure and integrating these technologies into real-world transport systems

Sustainable propulsion systems are central to addressing the transport sector’s climate, air quality and energy security challenges. China and Japan dominate global patenting activity in sustainable propulsion, particularly in battery and electric drive technologies driven by robust national strategies, industrial capabilities and R&D ecosystems. China leads with over 44,000 patent family publications in electric propulsion from 2000 to 2023, while Japan follows with more than 31,000.

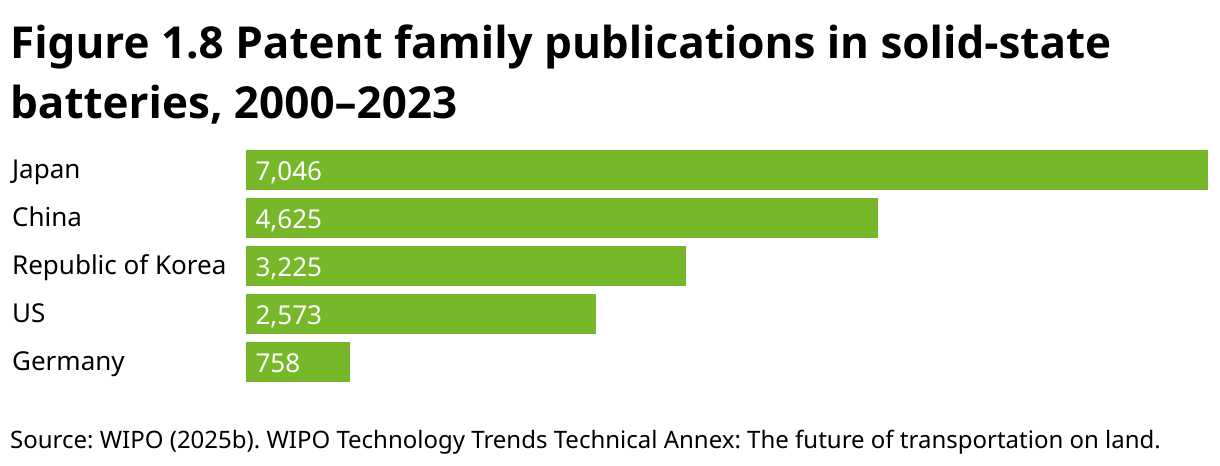

Among corporate players, Toyota Motor leads in patent family publications for batteries, electric propulsion and hydrogen/fuel cells with more than 26,000 patent families published since 2000, while China is the technology leader in device-to-device communication, navigation and cloud technologies. Patent activity in solid-state batteries has surged over the past decade, driven by growing R&D efforts across industry and academia, especially in China, Japan and the Republic of Korea. With over 7,000 solid-state battery patent families published between 2000 and 2023, Japanese inventors accounted for nearly 40% of all filings in this field (figure 1.8).

In parallel, Asian inventors are actively exploring alternative sustainable fuels – including biofuels, synthetic fuels and liquefied natural gas (LNG) – which can complement electrification by reducing emissions in sectors less suited to battery power

Rapid ascent in predictive and autonomous technologies for precision agriculture

Patents within the agrifood sector comprise more than 3.5 million published patent families (inventions) filed over the past 20 years. Asia continues to assert its leadership in agricultural innovation. Interestingly, with respect to energy technologies, recent patent growth within the AgriTech subdomain (one of two under agrifood, alongside FoodTech) is driven by rising interest in automation and IoT-based solutions. The most dynamic areas of innovation include connectivity, sensors, smart farming systems, precision agriculture and mapping/imagery. Japan, second only to the United States of America, is a leading inventor location in multiple IoT-related technologies such as robotics and drones, economic and whole farm management software, livestock management and carbon farming, thus demonstrating its pivotal role in the digital transformation of agriculture. Patent filing data reflects this momentum as China leads Asia with 137,000 international AgriTech patents, followed by Japan (107,709), the Republic of Korea (64,099) and India (53,766). These are largely driven by agricultural machinery makers, agrochemical firms and tech giants such as Sony, LG and Samsung

Asia continues to assert its leadership in agricultural innovation

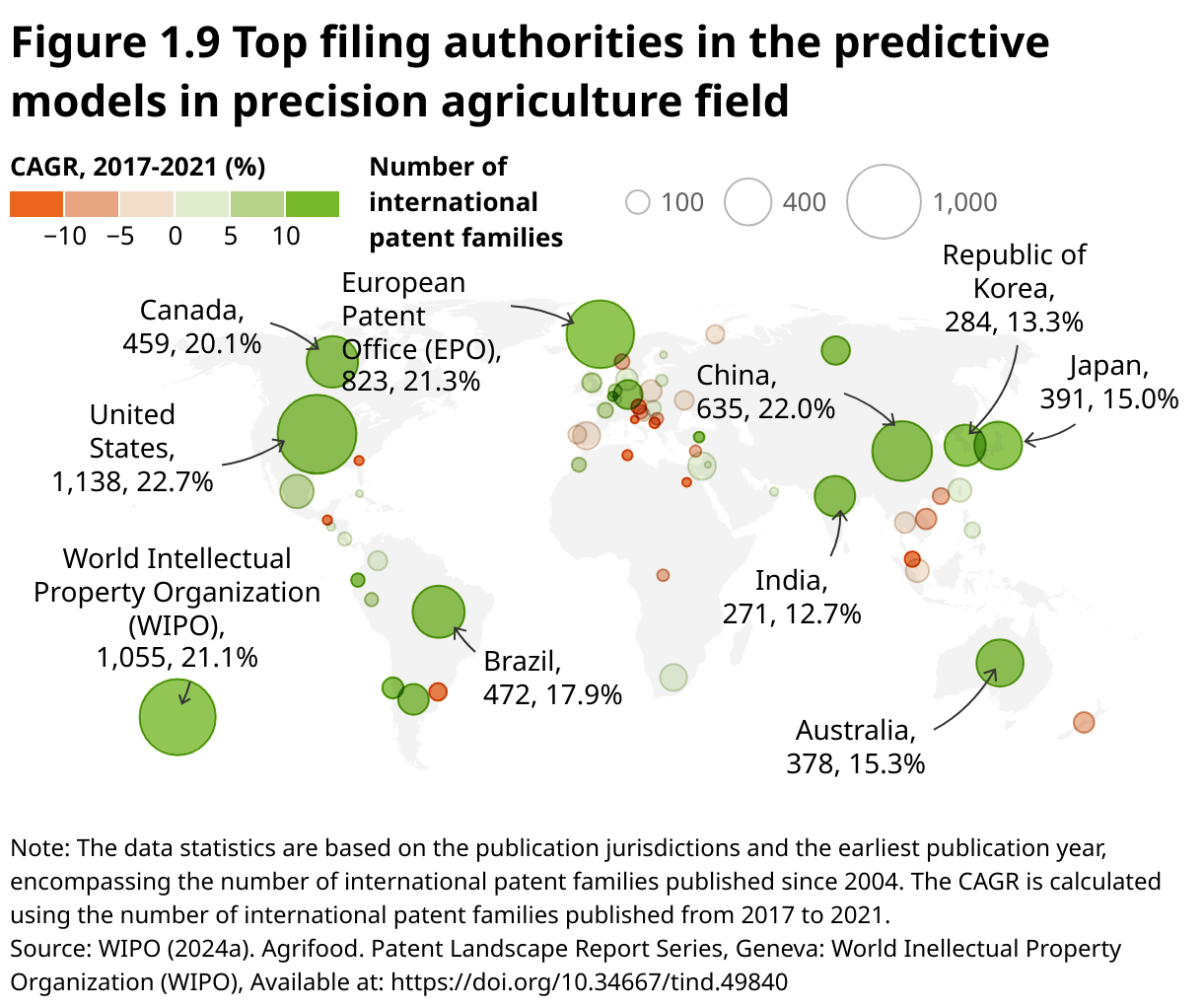

One of the top four key research hotspots in AgriTech identified by WIPO is precision agriculture, including advancements in robotic/autonomous agriculture vehicles and automation through AI and software. Data analysis from 1,500 IPFs in the predictive models in the precision agriculture field shows a significant recent annual growth rate of 27.1%, underscoring increasing global interest within the topic sector. Figure 1.9 shows that Asia is a strong contributor to this trend, with China leading at 635 international filings, followed by Japan (391) and the Republic of Korea (284). Australia also stands out regionally with 378 filings. These innovations reflect Asia’s growing commitment to sustainable and data-driven agriculture. Countries such as Bhutan, India and Viet Nam, are actively promoting digital technologies and smart farming systems – ranging from AI-driven advisory apps and carbon footprint tracking to weather warning platforms and digital traceability systems – to modernize agriculture and enhance productivity across diverse agro-ecological zones

In the domain of autonomous devices in precision agriculture, Asia is a key player, with rapidly growing use of technologies in soil management, crop harvesting and food processing

In the domain of autonomous devices in precision agriculture, Asia is a key player, with rapidly growing use of these technologies in soil management, crop harvesting and food processing to enhance efficiency and productivity across the sector. China tops the list with 1,379 international patent filings, followed by Japan and the Republic of Korea. Regionally, R&D output in Asia is substantial, with 1,177 IPFs focusing on autonomous agricultural technologies. The strong momentum in both predictive models and autonomous devices indicates Asia’s strategic investment in agricultural automation and smart farming, positioning the region as a hub for future-ready agrifood systems