The income approach, also known as the discounted cash flow (DCF) method, is a widely used technique for assessing the value of IP. It does this by estimating the expected future income or cash flow resulting from the development and commercialization of the IP.

Cash flow is the movement of money in and out of a company, typically for the purpose of developing, producing and selling goods and services. A cash flow statement summarizes a company’s cash inflows and outflows over a specified period. When using the income approach to valuation, an intimate understanding of the following factors is necessary.

The technology development plan – costs, timelines, limitations, infrastructure needs, etc.

The technological risks associated with commercializing the technology – the likelihood that the technology does not function as required in an industrially relevant setting.

Market/commercial risks – relating to regulatory approval, competition, technology obsolescence, litigation, etc.

The appropriate discount rate to apply to cash flows – a measure of the company’s cost of capital and the probability of success (or risk of failure).

The remaining useful lifetime of the IP – while the lifetime of an IP is typically based on when it expires, the IP can have utility beyond this point, if the underlying technology is buoyed by valuable know-how and trade secrets. The lifetime of the IP can also be extended; for example, through building a strong brand or by filing follow-on patents. Conversely, in fast-moving industries the remaining useful life can be shorter than the formal protection period due to technology obsolescence.

Using the income approach, there can be a wide range of outcomes, particularly if the IP can be deployed in several industries, or in products of different formats, features and applications. For example, case study 2 on battery technology, described in the market approach above, may have applications in several sectors including automotive, aerospace, consumer electricals, satellites and medical devices. The value of the IP in each of these sectors will be different, depending on assumptions made regarding the market development of the IP, and expected sales.

Advantages

Valuation uses relevant available data from the buyer, which reveals their capabilities (projected development budgets, markets of interest, production and sales, etc.).

The approach allows for a large degree of flexibility in incorporating assumptions and building scenarios.

Valuation allows for risk adjustment that considers the probability of attrition during development. as well as the uncertainty of future costs and income.

The approach is well established and is favored by valuation professionals.

Disadvantages

It is difficult to incorporate the unpredictability of future events.

When a TTO uses the approach, it often assumes cash flows to be static over a specified time horizon, which may not be the case.

(2)TTOs typically do not use techniques that account for detailed growth or erosion models and complex probability weighting. In contrast, large companies with diverse IP and product portfolios are often well versed in such techniques, and will leverage them in negotiations with academic institutions. From the perspective of a TTO, the approach does not account for management flexibility. For example, management staff have the opportunity to stop, pivot, sell, license or abandon the development of a technology as they receive new information on the market, technology performance and other factors.

All risks are typically grouped together, and adjusted for in the discount rate applied and the probability of success estimations. Often, risks may need to be untangled to identify different impacts such as risk of litigation, technological risk, infringement or piracy.

The approach does not adequately account for the fact that products on the market may rely on several IP rights and may also have freedom to operate dependencies.

Finding relevant data to populate models on discounted cash flow

Populating DCF models requires the valuer to source, sift and analyze vast amounts of information concerning IP-related deals available from the parties involved in the valuation (IP owner and IP seeker). Useful data sources include the following:

Market intelligence reports focused on products incorporating the IP under evaluation, in the industry sectors of interest.

Company annual reports often include information on costs (under R&D investment), particularly if the focus is on a highly visible and novel technology.

Peer-reviewed publications, patents and books.

Reports from industry associations, non-governmental organizations, statistical bodies, governments, and world bodies such as the World Health Organization, the United Nations, and the Organisation for Economic Co-operation and Development.

Technology reports, blogs, magazines and white papers tend to be written by technology enthusiasts with intimate knowledge of the development processes for new technologies. These publications can help you engage with key opinion leaders as well as potential buyers or licensees.

Mandated disclosures to regulatory bodies.

Outcomes of court cases where IP infringement, ownership, sharing of exploitation benefits and other issues have been contested.

Discussions with companies (IP buyers or licensees) in sectors of interest. This is one of the most powerful ways to obtain relevant information on potential buyers’ plans, capabilities and strategies. To obtain this information, it is important you establish good working relationships with interested companies.

Subscription databases and business intelligence services.

Discussions with experts and key opinion leaders in your network, particularly those with insights into developments in the technology space of relevance to your IP. These individuals may be researchers in academia, subject area experts in industry (typically research managers or directors) and regulators. Key opinion leaders tend to have intimate knowledge of the potential costs of development to market, market dynamics and other useful information.

Using the income approach

When using the income approach, you may find it useful to take the following steps.

Step 1: Carry out due diligence, engage networks and conduct market research – for this step, it is important to have a fundamental understanding of a potential buyer or licensee’s capabilities and plans, including:

Their technology development plans, such as costs, timelines, milestones and resources to be committed.

Their capabilities, including market capitalization, financial background, reputation, commercial strategy, company maturity, geographic reach and markets covered.

Their exposure to risk, including technological, market and legal.

Their understanding and perception of the utility of the IP, including features, benefits, limitations and durability.

This information allows you to profile the potential buyer and use this information to develop a DCF format (covering time horizons, types of benefits and costs, discount rate to use, etc.).

When engaging your network, recognize that professional contacts such as peers in TTOs, key opinion leaders and other experts can provide useful insights to inform your DCF model – with information such as expected technology development costs, timelines and risks, pertinent regulations (standards, certifications, restrictions) and market dynamics (trends, drivers, risks, challenges).

Complement insights gained with market intelligence such as information from market report providers and subscription databases – to better understand market characteristics, industry dynamics, industry standards and discount rates.

Step 2: Determine cash flows (in and out) – by populating the cash flow model with the information collected, focusing on:

Cash inflows, including investments in the development such as own funds provided, translational research grants, and investment from business angels and venture capital, as well as expected sales of products incorporating the IP.

Cash outflows that are incurred as a consequence of commercializing the IP, including:

Development costs, such as salaries, raw materials costs, equipment and estate costs.

Sales and marketing costs.

General and administrative costs.

Overheads, as costs incurred by virtue of developing the technology. Often, these are a percentage of sales, which can be difficult to determine for a new company (spin-out) created to commercialize specific IP, but more predictable for a well-established company with robust processes or for developing late-stage IP in a well-structured sector such as biotechnology or the pharmaceutical industry.

Assumptions. Since cash flows are forward-looking, it is inevitable that certain assumptions are made with respect to expected sales, growth forecasts, market penetration and other factors. These assumptions should be minimized wherever possible and based on defensible reasoning. As far as possible, note and make explicit all key assumptions made.

Net cash flow. The difference between all cash inflows and all cash outflows for a particular period (e.g., one year of operation) is the “contribution”. The contribution is often negative in the pre-market period, owing to the costs of technological development. Similarly, contributions become positive once the product enters the market and revenues are generated.

Step 3: Discount contributions for each cash flow – and calculate the sum of all DCFs to determine the NPV of the IP. Discounting refers to the process of determining the present value of an IP opportunity, which is realized at a future date. The discount rate applied to a cash flow primarily reflects the risks involved in developing the opportunity, the technology developer’s capabilities, the cost of borrowing in the sector, and the evolution of the sector in general (new and fast-growing or steady and stable).

Aswath Damodaran has compiled useful datasets to support discount rate estimation for several sectors and regions.

Step 4: Risk-adjust the DCF model – as technology development is an inherently risky endeavor. An IP may fail to reach the market for several reasons, including but not limited to:

Failure to perform as required in an industrially relevant setting.

Failure to attain regulatory approval.

Costs of development exceeding expectations and budgets.

Competing solutions entering the market earlier and eroding the commercial opportunity.

IP obsolescence.

You therefore need to risk-adjust the DCF model to account for the probability of the IP successfully meeting development and regulatory milestones, and successfully selling in the market. Accounting for risk in this way yields a risk-adjusted NPV. Assumptions made to appropriately risk-adjust a cash flow model must be data-driven and based on verifiable information.

This exercise is more challenging in some sectors than in others. For instance, in the biotechnology and pharmaceutical industry, there is an abundance of data on attrition rates of drug candidates during clinical trials and at the regulatory review stages. By contrast, obtaining similar information for IP in other sectors such as the physical sciences is more challenging. It is therefore crucial that values used in the cash flow model are sense-checked with colleagues and valuation professionals and during discussions with a potential buyer.

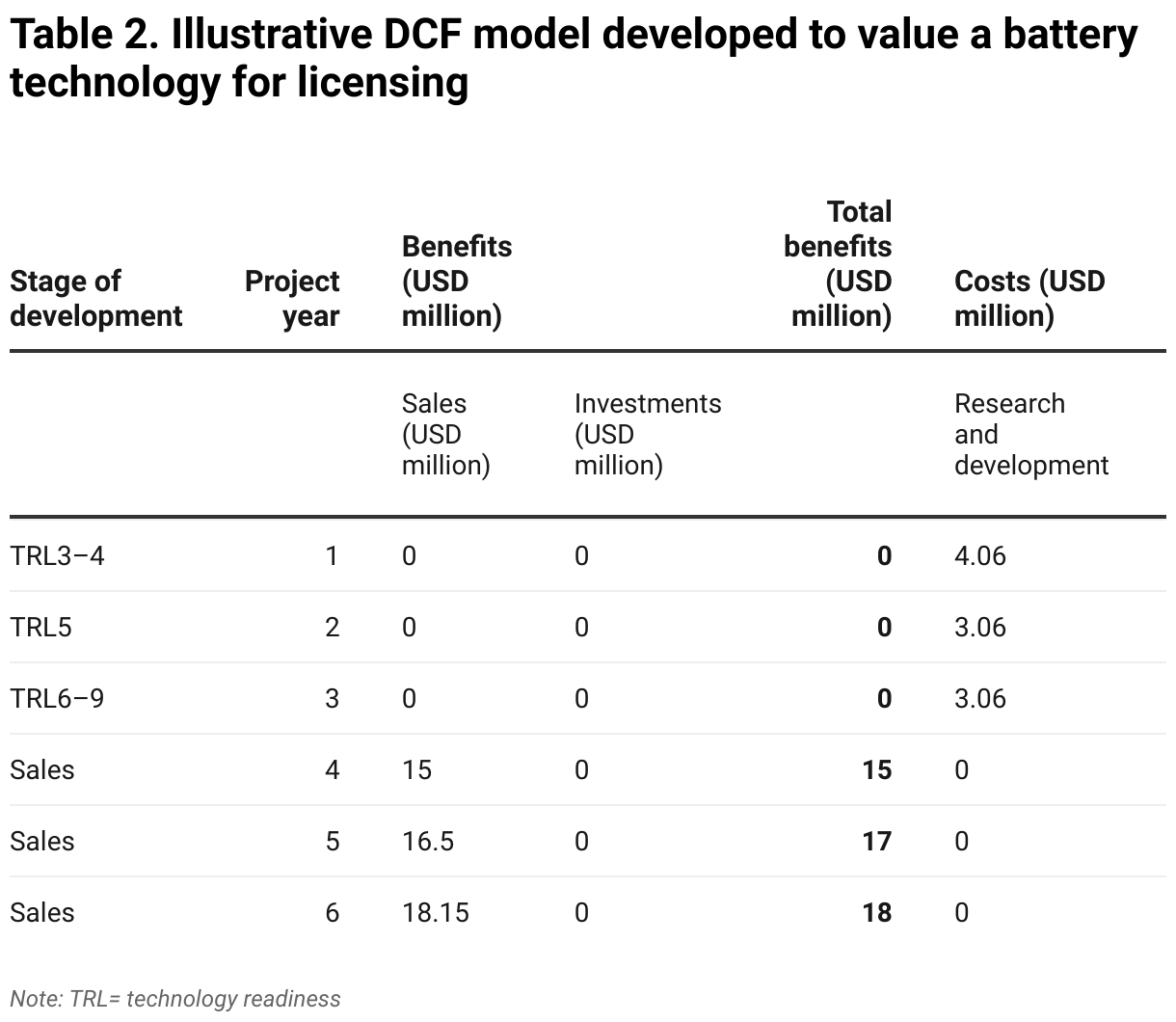

The battery technology described in the market approach was also valued using the income approach. It is important to note that while applying the DCF model in this case, we are valuing not only the technology but also the business of selling batteries in an existing market.

The TTO identified an automotive company that was keen to in-license the IP and carried out due diligence on a potential licensee. It established that the company was a mid-sized enterprise with an annual production capacity of 500,000 car batteries per annum. The company had been formed as a joint venture between an automotive company and a well-established battery supplier. It had established premises, equipment and a production plant, and was led by a specialist engineering team. This team had extensive experience in developing novel battery technology and transferring this technology to manufacturing, in a range of electro-chemical products and formats (cells, battery packs and other applications).

The TTO identified that the company had modest sales projections, of 10 percent growth per year, and that batteries were the only product it produced and sold. The company exclusively supplied a large established global automotive company which bought all the stock produced. The TTO then obtained the following insights from key opinion leaders and market intelligence:

IP maintenance – the licensee pays 100 percent of maintenance and renewal fees on the patents in all territories.

Development costs – insights including:

The cost of R&D in developing the IP is approximately USD 10 million, frontloaded in the first three years of development. These costs may fluctuate depending on the number of batteries produced.

Post-launch R&D costs are approximately 0.01 percent of sales.

Cost of goods sold is approximately 15 percent of sales.

Sales and general and administrative costs are approximately 10 percent of sales.

With regard to risk adjustment, there was no consensus among key opinion leaders. The experts used a diverse range of approaches to model possible outcomes and scenarios. As a result, it was difficult to account for risk adjustment in a way that allowed the TTO to defend its valuation estimates. This meant that the DCF model developed was not formally risk-adjusted. Instead, the TTO engaged with interested parties to ascertain their perception of risk when taking the battery IP to market.

This outcome is relatively common with TTOs, which may address an information shortfall by working with their network of industry insiders to develop a well-informed view of the risks associated with technology development in areas where the TTO holds IP that can be commercialized.

In this case study, the TTO used the information collected to develop a DCF model, as shown in Table 2.

Having obtained an estimated IP value for the DCF model, the TTO refined it further via discussions with interested buyers, some of whom willingly shared information to facilitate risk adjustment. Ultimately, risk-adjusting the valuation model will typically shrink the value of an opportunity.

Ensure that you have a realistic view of the capabilities of the company that will develop the IP to market.

Understand and apply an appropriate discount rate that combines:

The project-specific risk profile (e.g., a university spin-out is considered high risk compared to a well-established company with a strong track record of developing IP to market).

The probability of success, which accounts for technical, legal and market risks.

Understand that this approach is favored by valuation professionals in industry, investors and analysts. It can be powerful if used appropriately by IP owners seeking to license or raise funds for their IP.

Remember to adapt to your local norms and values that align with your target region or market, with respect to risk adjustment, discount rates, time to market, etc.

Use the market approach or cost method to provide a comparative view of value wherever it makes sense.