Key trends and insights

Co-published annually by the World Intellectual Property Organization (WIPO) in partnership with the Luiss Business School (LBS), this second edition of the World Intangible Investment Highlights (WIIH) reveals that intangible investment in the global economy has grown well over three times faster than tangible investment since 2008, despite economic headwinds and business uncertainty.

Investment in intangibles – such as software and databases, intellectual property (IP), research and development (R&D), brands and design (see box 1) – now constitutes a large and growing share of world gross domestic product (GDP). Leadership in the global intangible economy is multifaceted: the United States of America (US) dominates in terms of absolute investment, Sweden leads in terms of intangible investment intensity (i.e., intangible investment as a share of GDP) and India has recorded the fastest growth. Software and data emerges once again as the fastest growing category of intangibles and this year’s special theme elaborates on the linkages between artificial intelligence and intangible and tangible investment (see box 2).

The WIIH 2025 and its underlying Global INTAN-Invest Database (July 2025) provide unprecedented statistics on cross-country investment – both annual and quarterly – spanning 27 high- and middle-income economies, including updated estimates for India (until 2022) and Japan (until 2023), and first-ever estimates for Brazil. Together, these 27 economies accounted for more than half of global GDP in 2024. The dataset covers all intangible asset classes, including those assets not yet included in official statistics, thus helping to bridge data gaps and facilitate evidence-based policymaking (see annex).

The seven stylized trends in intangible investment for 2025 are as follows.

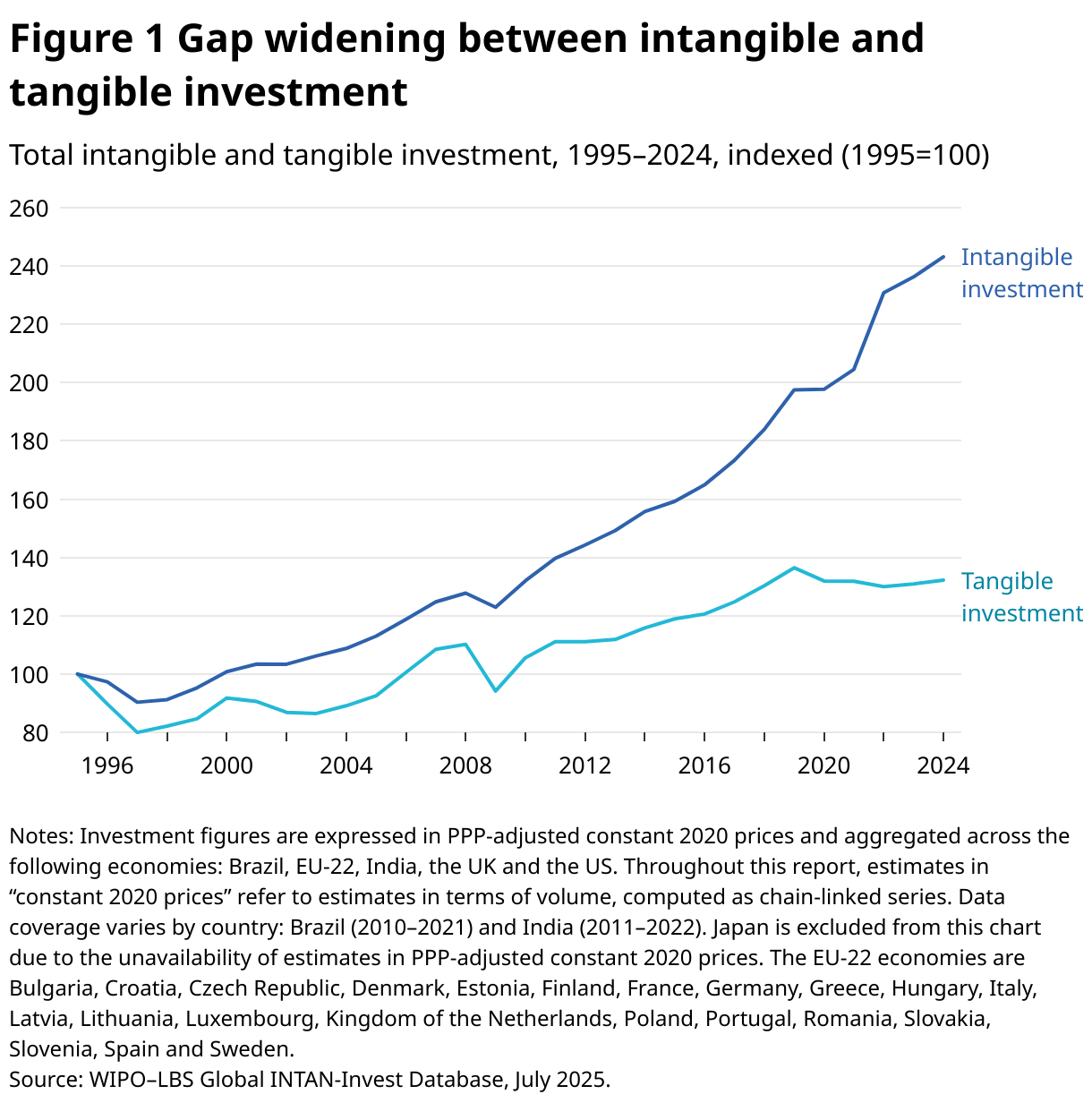

Stylized trend 1: Intangible investment grew well over three times faster than tangible investment between 2008–2024

Among the 27 economies covered by this report, intangible investment has been consistently outpacing tangible investment over time (figure 1).

A significant turning point came around 2008, when intangible investment began to accelerate, ultimately achieving a compound annual growth rate (CAGR) of about 4.1 percent between 2008–2024. This growth rate has far surpassed that of tangible investment, which expanded by only about 1.1 percent over the same period. This has meant that intangible investment has grown well over three times — 3.7 times to be precise — as fast as tangible investment between 2008-2024. In the last year alone, intangible investment grew by nearly 3 percent between 2023–2024, compared to a tangible investment growth of 1 percent.

What are intangible assets? Today's most valuable companies derive their competitive advantage not from physical capital, but from intangible assets – such as R&D, software, data, design, branding, organizational know-how and skilled talent, all creating substantial economic value.

Why do they matter? Intangible assets drive competitive advantage, innovation and customer loyalty in a knowledge economy. Though invisible, they fuel economic growth, create high-paying jobs and improve living standards.

Why measure them accurately? Despite their critical importance, intangible assets remain poorly understood and under-measured. Precise measurement is essential for identifying growth drivers and designing effective policies. Poor measurement leads to undervaluation, capital misallocation, underinvestment and, ultimately, misguided policymaking.

The divergence in growth between tangible and intangible investment has widened in recent years. Tangible investment has remained almost flat since 2020 amid tightening monetary policies and global economic uncertainty, whereas intangible investment, across the economies covered in this report, has continued to climb, reaching USD 7.6 trillion (in current prices) in 2024, up from USD 7.4 trillion in 2023.

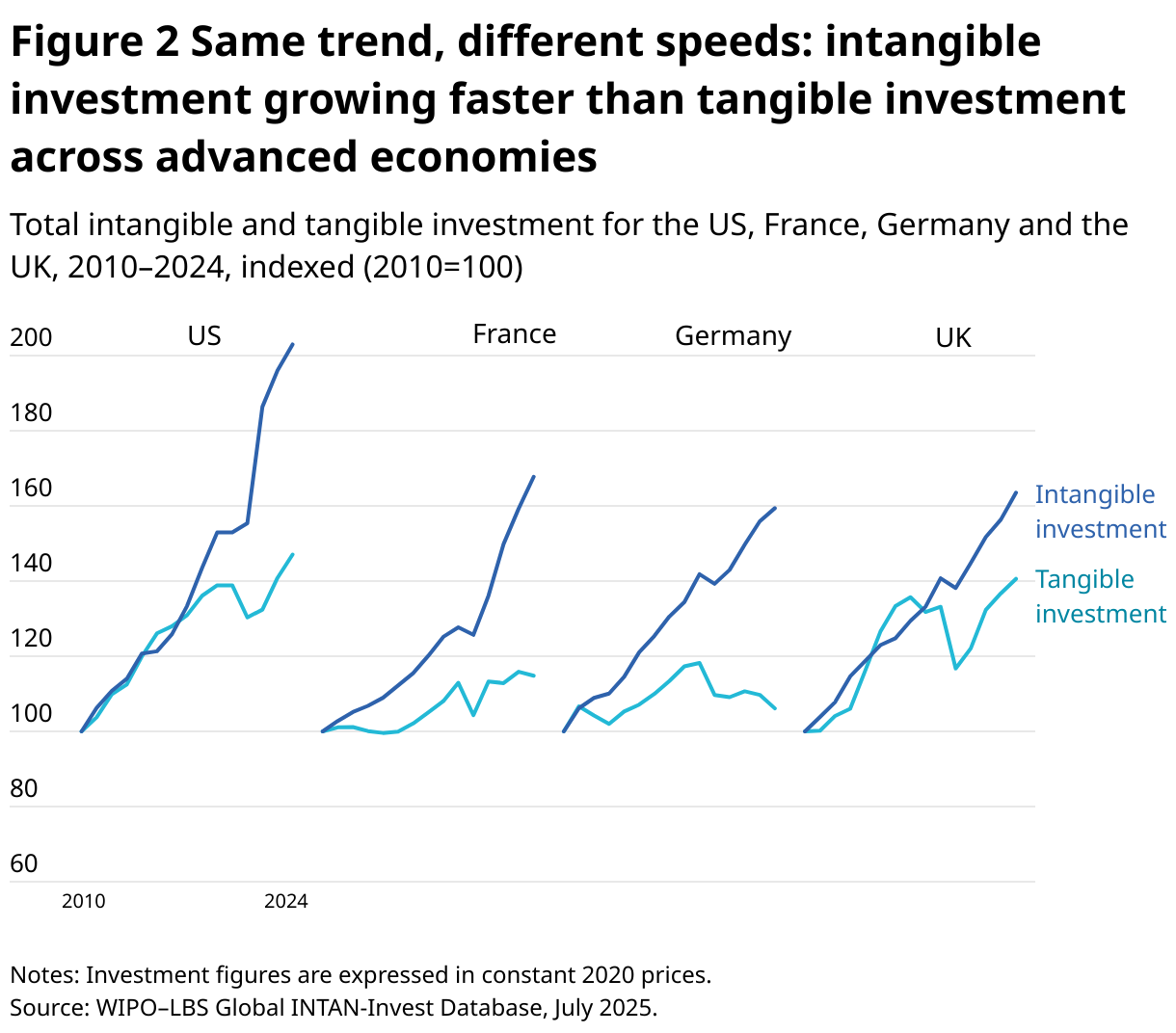

This same stark divergence in investment growth rates is evident across major advanced economies, as well as in Brazil and India. Across these countries, intangible investment has consistently outpaced tangible investment, a trend that has persisted even amid periods of slowing economic growth and low business confidence (figures 2, 3 and 4).

In the US, intangible investment grew more than five times faster than tangible investment between 2020–2024 (figure 2). France followed a similar pattern, with intangible investment increasing at a rate three times faster than tangible investment. This divergence is even more pronounced in Germany, where intangible investment increased by over 3 percent annually during the period, while tangible investment declined by about 1 percent. In the UK, on the contrary, tangible investment (growing at 4.8 percent) slightly surpassed intangible investment (which grew at 4.3 percent) during this period.

Based on the most recent data from 2024, among those economies with leading levels of intangible investment, France recorded the fastest growth in intangible investment in real terms (over 5 percent from 2023 to 2024), followed by the UK (over 4 percent), Spain and Denmark (both close to 4 percent) and the US (3.5 percent). Among economies with relatively lower levels of intangible investment, Lithuania stood out with a remarkable growth rate of nearly 17 percent between 2023–2024. In the case of tangible investment, the US led among economies with a relatively high tangible investment level, recording growth of over 4 percent between 2023–2024.

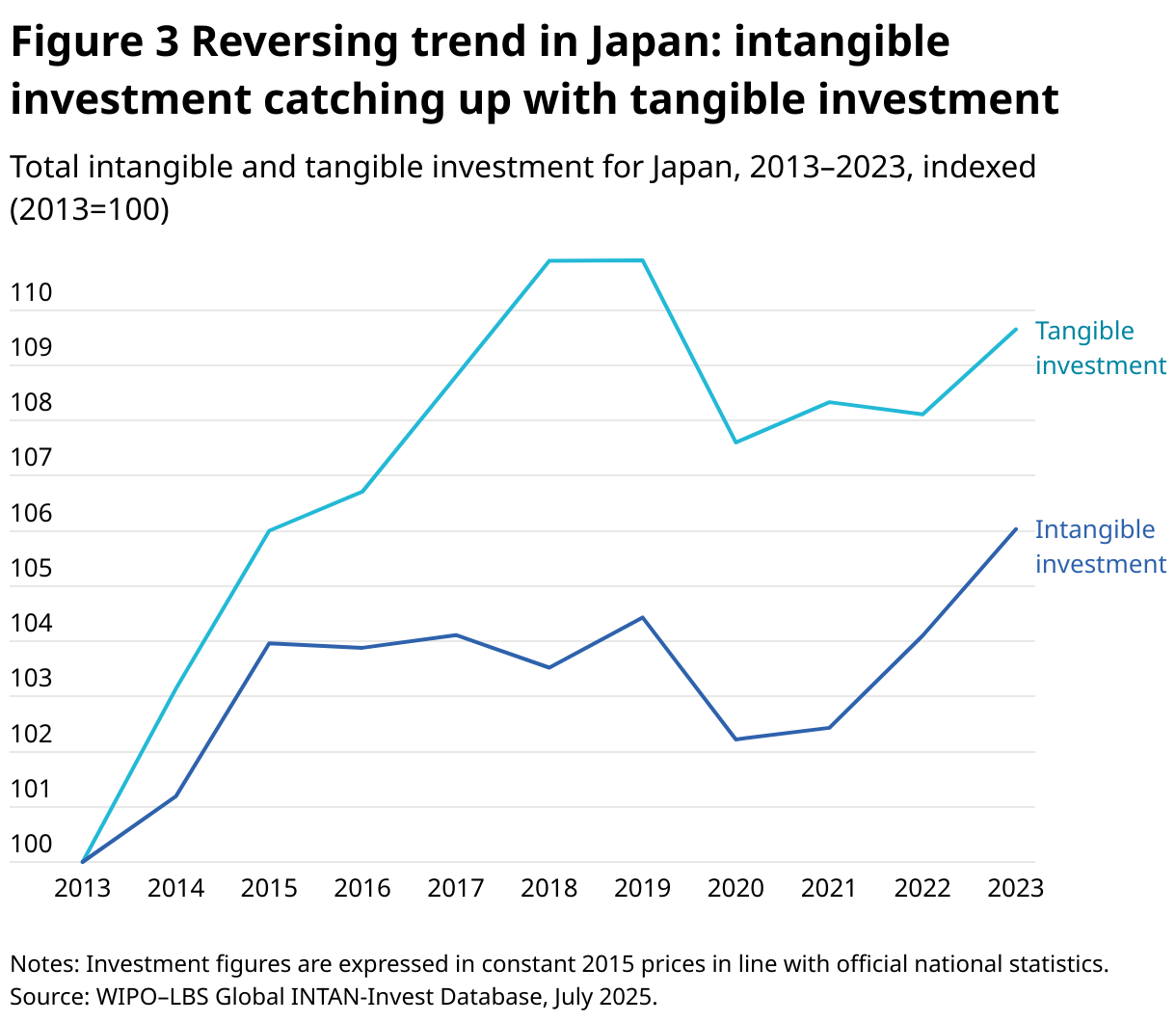

In the case of Japan, tangible investment has historically grown faster than intangible investment (figure 3). Based on updated data for Japan from 2013 to 2023, tangible investment recorded an average annual growth rate of approximately 0.9 percent. Intangible investment expanded more slowly during the same period, at a rate of 0.6 percent annually. Since 2020, however, this trend has reversed: between 2020–2023, intangible investment grew at the faster pace, averaging 1.2 percent annually compared to 0.6 percent for tangible investment.

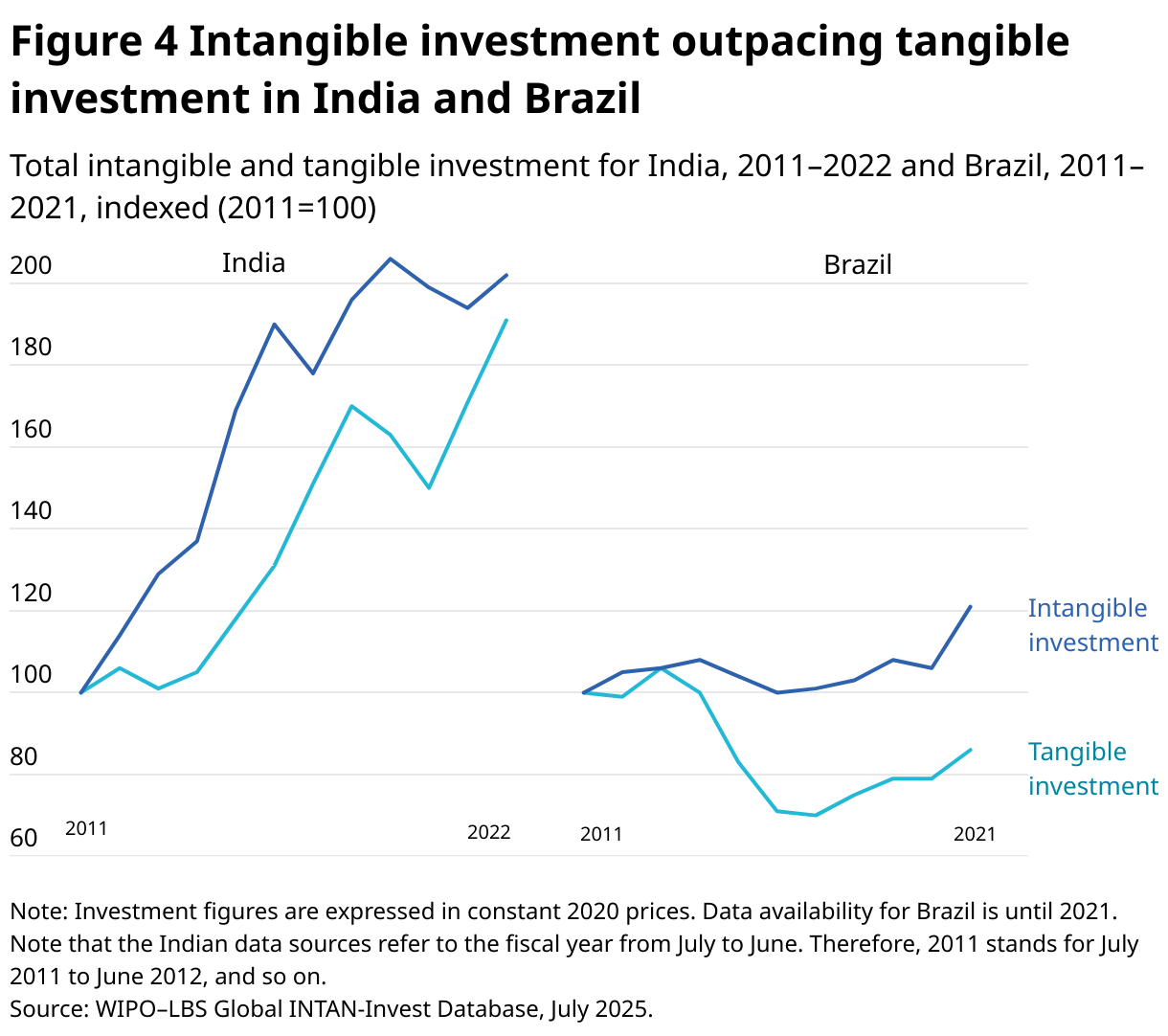

Figure 4 compares the pattern of growth of intangible and tangible investment across India and Brazil. In India, both investment types recorded steady growth rates between 2011–2022, with intangible investment increasing at nearly 7 percent annually – slightly outpacing tangible investment at around 6 percent. However, the gap has narrowed since 2020, driven by an acceleration of tangible capital formation. The latest data for India show that in 2021–2022, intangible investment grew by 4 percent, whereas tangible investment grew faster at close to 12 percent.

In Brazil, investment trends diverged between 2011–2021, with intangible investment growing at nearly 2 percent annually as tangible investment declined by over 1 percent. The most recent data show that between 2020–2021, Brazil’s intangible investment surged at 14 percent, whereas tangible investment grew at 8 percent.

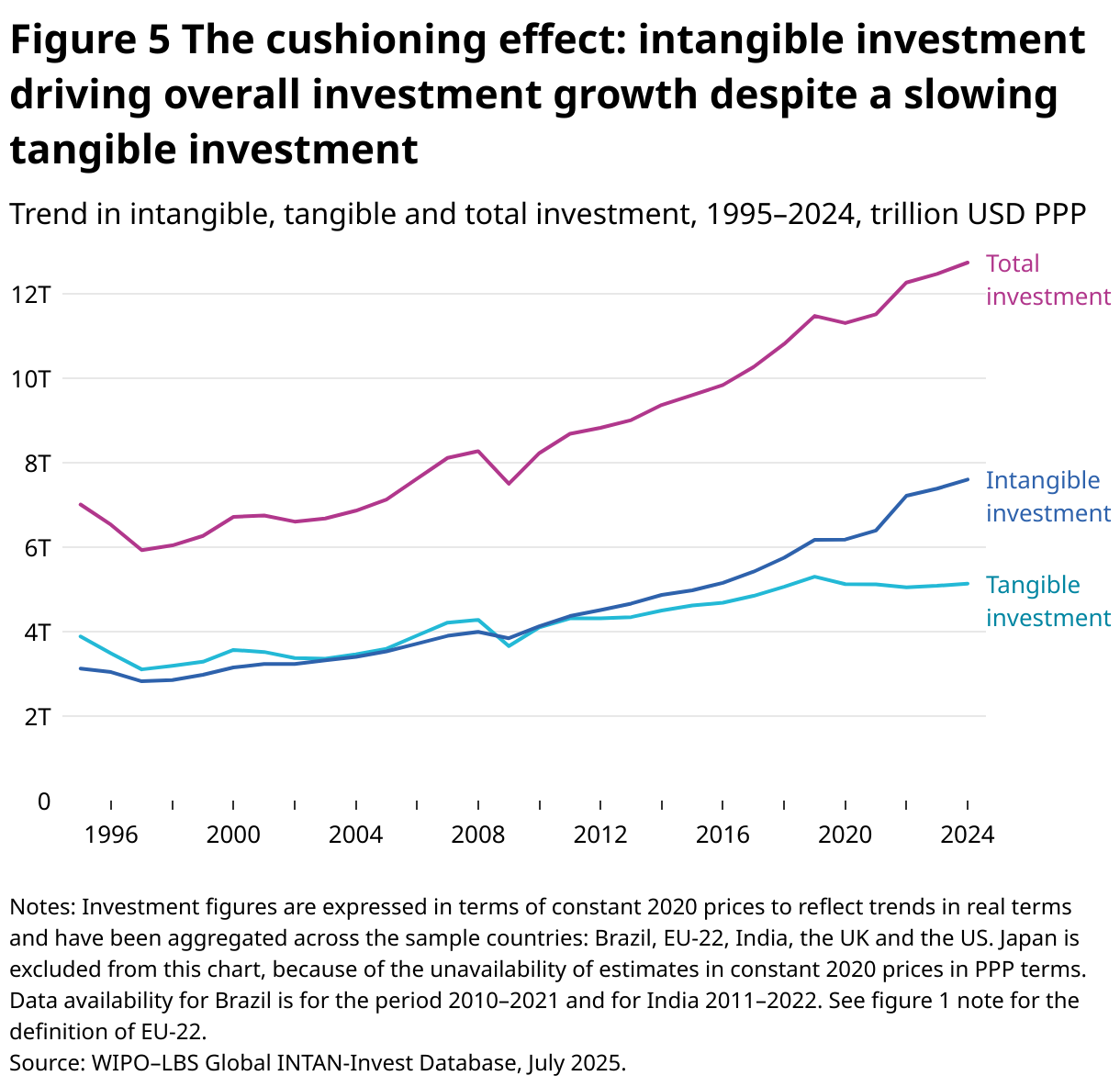

Stylized trend 2: Intangible investment growth has cushioned an overall investment slowdown amid sluggish economic recovery and high interest rates

Despite macroeconomic headwinds – including inflationary pressures, interest rate hikes and declining tangible investment – total investment has maintained steady growth, driven by intangible capital formation (figure 5).

This trend of intangible investment driving overall growth in total investment is even more pronounced in the most recent year. Between 2023–2024, intangible investment expanded by nearly 3 percent, increasing from USD 7.4 trillion to USD 7.6 trillion (in current prices), whereas tangible investment grew by just 1 percent, from approximately USD 5.08 to USD 5.13 trillion. As a result, total investment grew by over 2 percent in real terms, from USD 12.5 trillion in 2023 to USD 12.7 trillion in 2024.

Persistent growth in intangible investment has therefore partly offset what would otherwise have been a more severe investment shortfall, and by extension, helped support productivity growth. The International Monetary Fund's April 2025 World Economic Outlook (p.5) points to chronic underinvestment as a key reason for labor productivity having slowed since 2010, stating that “Capital shallowing because of chronic investment weakness can explain roughly half of the productivity growth slowdown in advanced economies and about a third of that in emerging market and developing economies."

In this context, the acceleration in intangible investment has played a mitigating role. While investment in machinery, equipment and buildings has stagnated, firms have kept investing into R&D, software, data, and organizational capabilities. Such intangible assets not only support capital deepening, but also contribute to disembodied productivity gains – particularly within services and AI-intensive sectors.

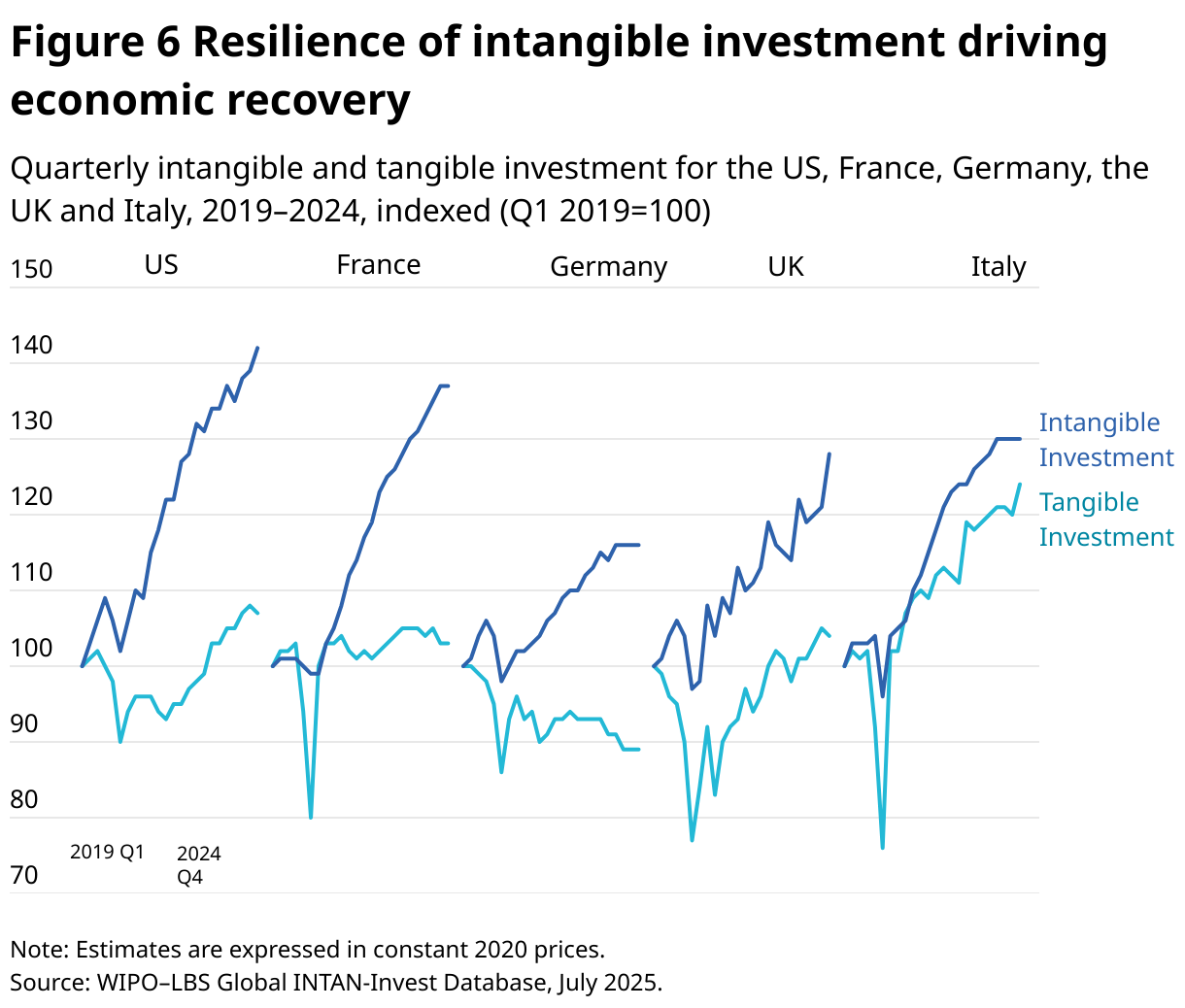

Country-level quarterly data serve to illustrate this dynamic since 2020 (figure 6).

In Europe, the picture is more mixed, although intangible investment is seen to generally outpace tangible investment (figure 6). France mirrors the US dynamic in having stronger intangible growth. In the UK and Italy, both investment types have grown at a similar rate. In Germany, total investment growth since 2020 has been mainly driven by intangibles, which have counterbalanced a declining tangible capital accumulation over time.

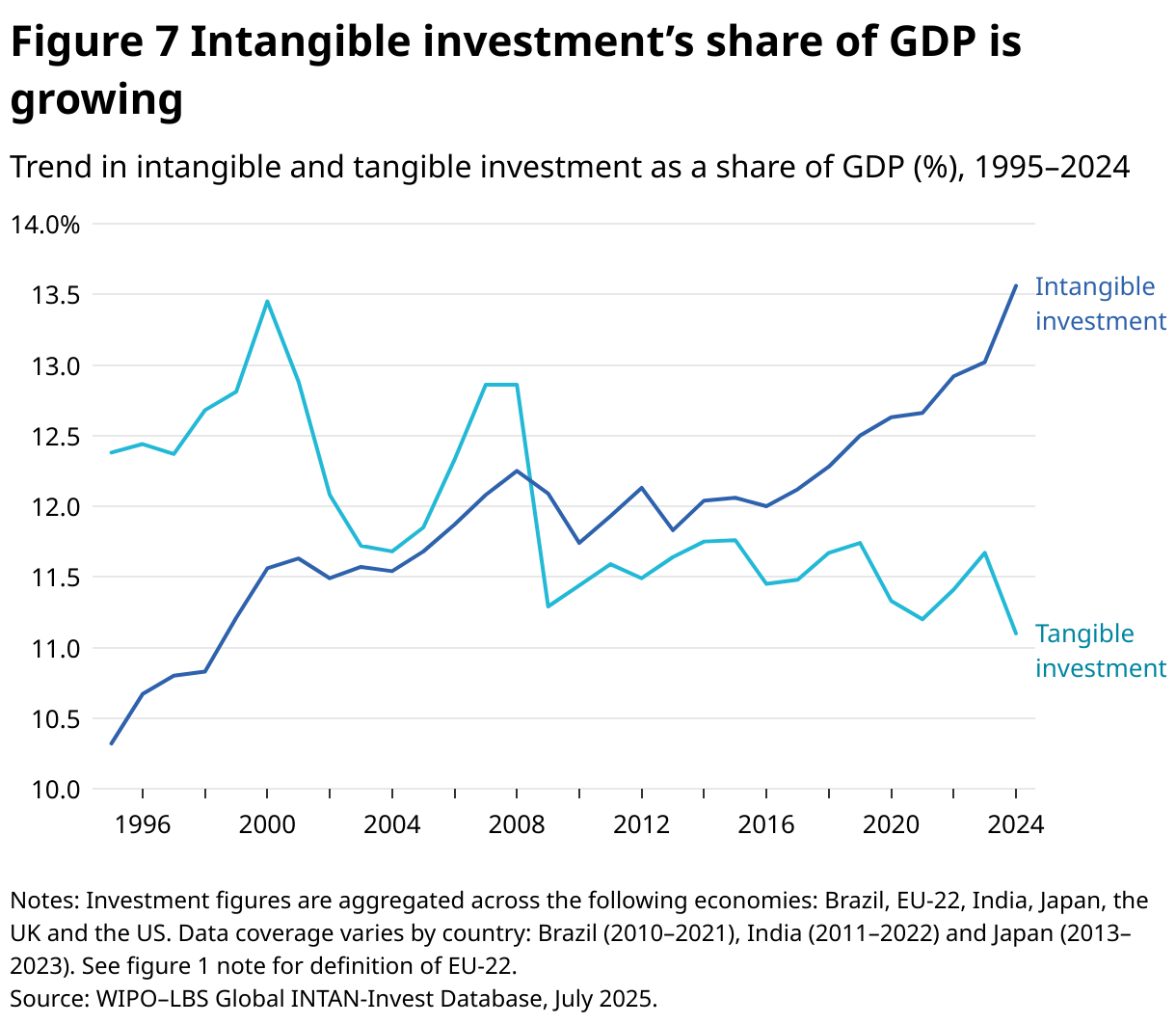

Stylized trend 3: Intangible investment constitutes a growing share of GDP, relative to tangible investment

The share of intangibles in GDP has been steadily growing over time (figure 7). From 1995 to 2024, intangible investment's share rose from about 10 percent to nearly 14 percent of total GDP (aggregated across sample economies), whereas tangible investment's share declined from 12 percent to 11 percent over the same period. Intangible investment (as a share of GDP) surpassed tangible investment (as a share of GDP) for the first time in 2009, and the gap has been widening since. In turn, the GDP share of intangibles increased from about 13 percent in 2023 to 13.6 percent in 2024, compared to 12.9 percent in 2022.

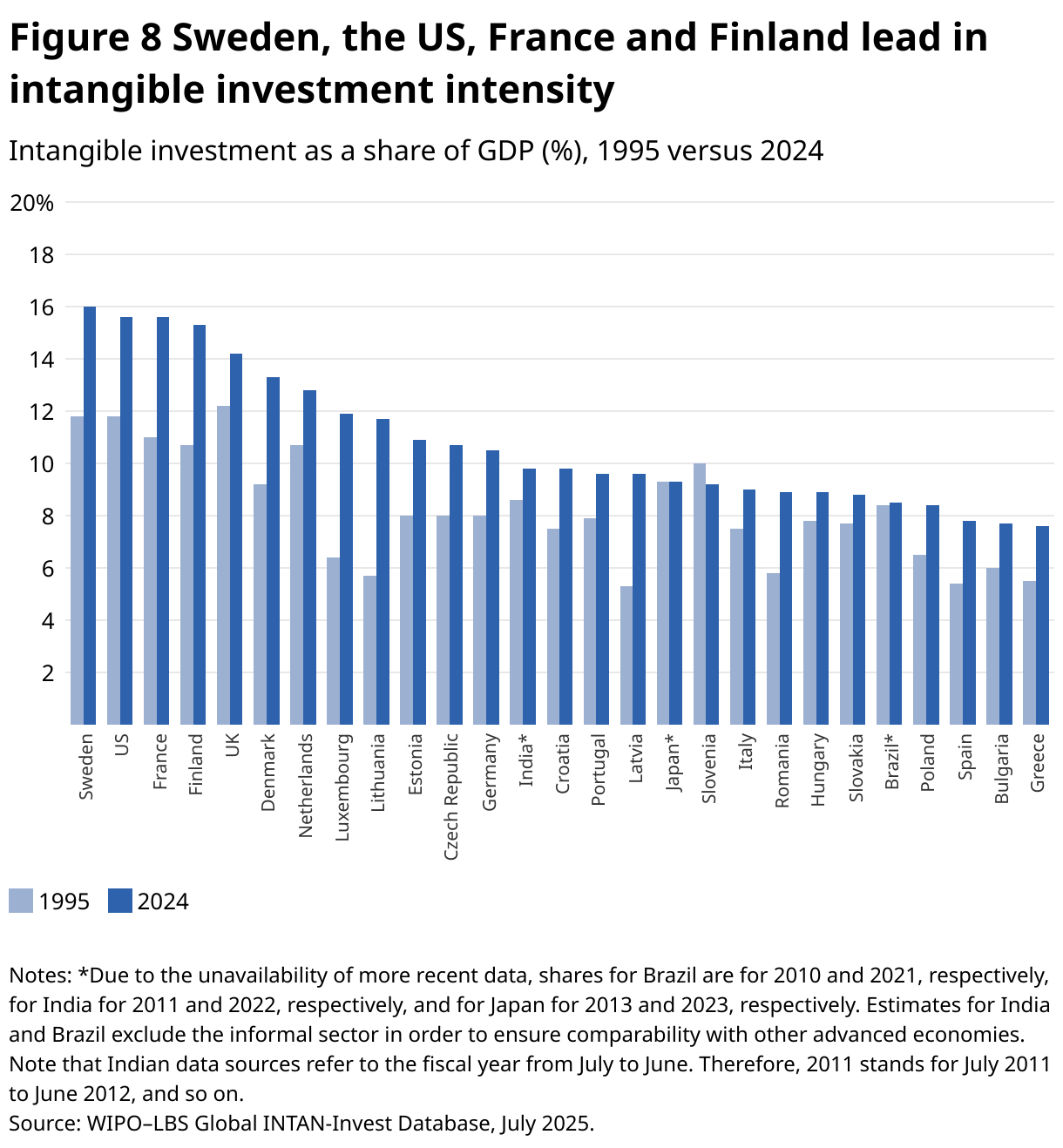

This trend is reflected at the country level. A comparison of intangible investment's share of GDP across countries shows that, in 2024, intangibles accounted for a larger share of GDP than in 1995 in all sample countries except Slovenia (figure 8).

In 2024, Sweden maintained its leading position as most intangible intensive economy, reaching 16 percent of GDP. Sweden was followed by the US, France and Finland, where intangible investment accounted for over 15 percent of GDP. India's intangible investment intensity (close to 10 percent) puts it ahead of several European Union (EU) economies, as well as Japan. Brazil's intangible intensity (8.5 percent) is comparable to that of Poland (8.4 percent), while surpasses that of Spain (7.8 percent) and Greece (7.6 percent).

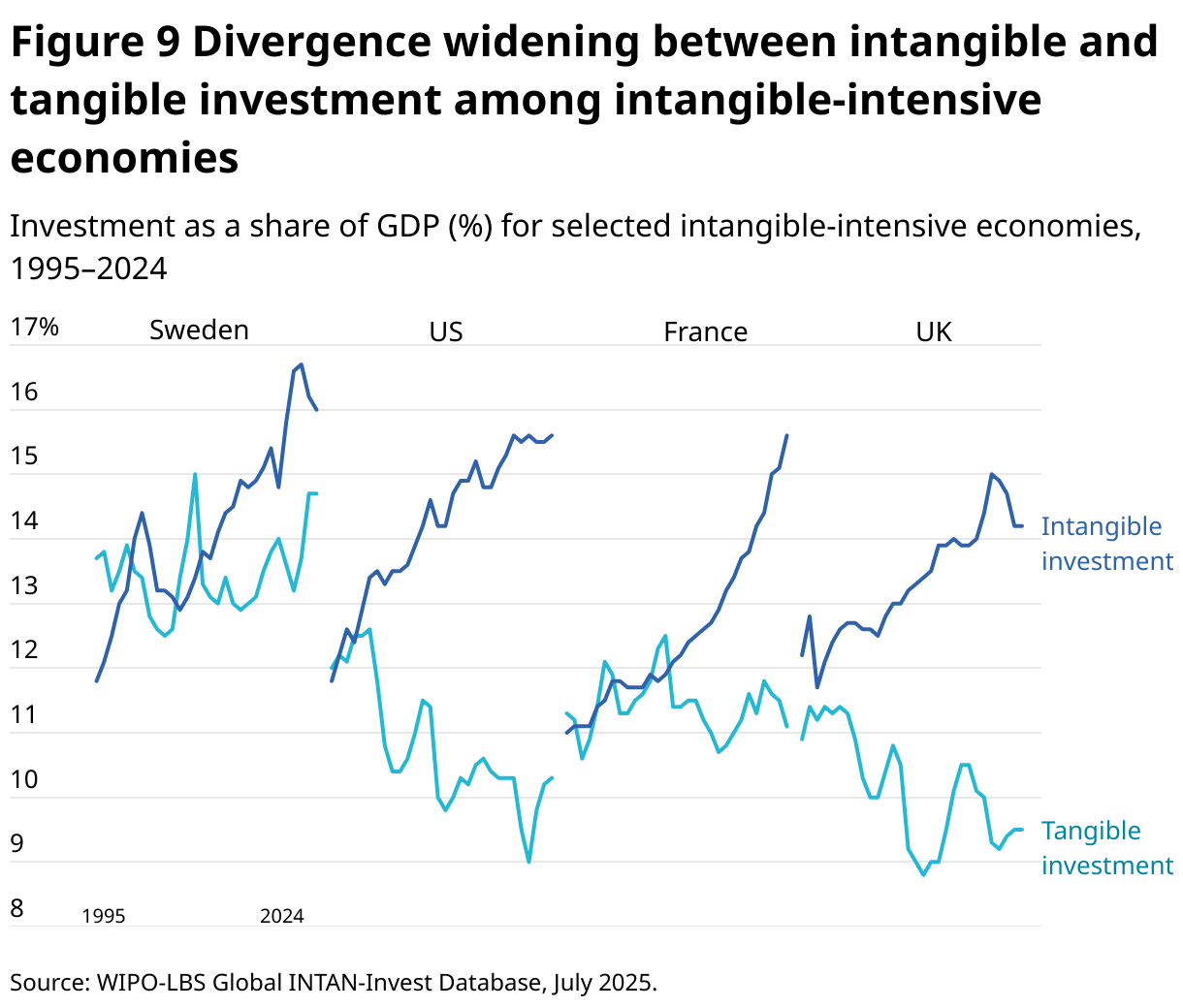

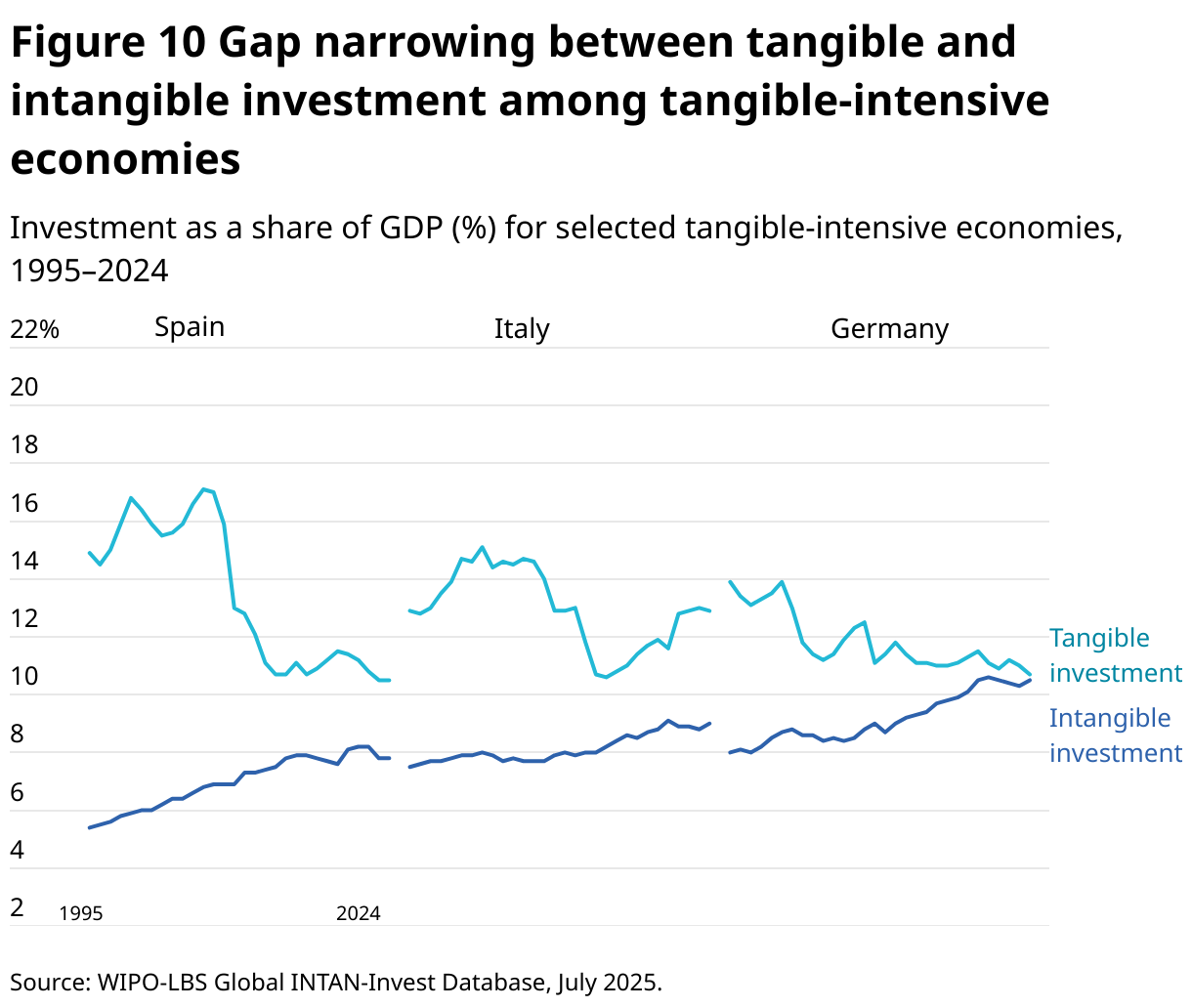

A key divergence is emerging between two types of economies. In those economies where intangible investment already dominates, the gap between intangible and tangible investment continues to widen (figure 9). Conversely, in those economies where tangible investment is still dominant, the trend is reversed: the gap is narrowing, driven by a faster growth in intangibles that signals a potential catch-up process (figure 10).

Japan is an exception that does not fit either pattern: while tangible investment has consistently accounted for a larger share of GDP, the gap between intangible and tangible investment intensity broadly remained stable between 2013–2023.

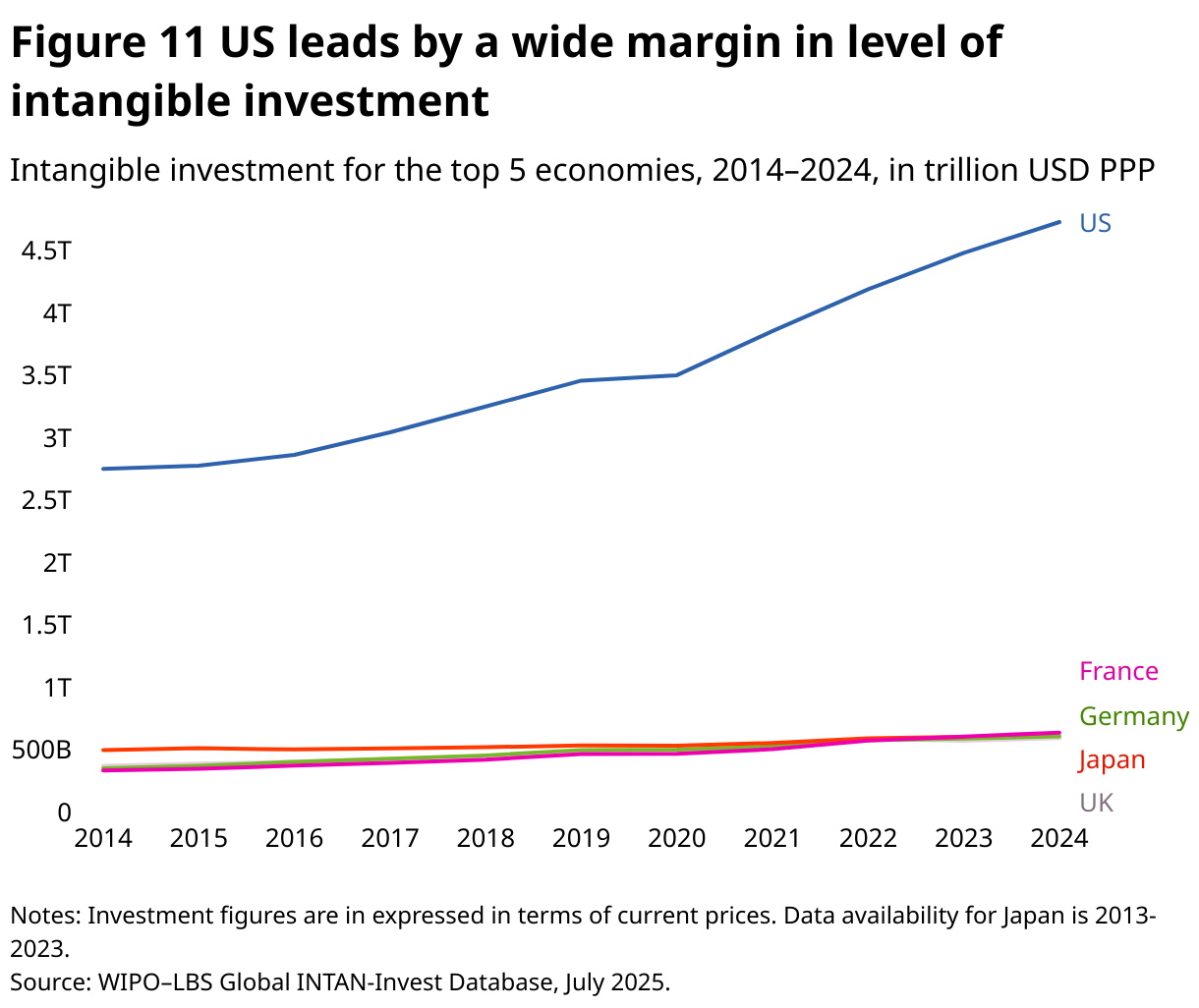

Stylized trend 4: The US leads in absolute level of intangible investment, with its 2024 level nearly twice that of France, Germany, Japan and the UK combined

The US remains the global leader in intangible investment by a substantial margin. In 2024, its intangible investment reached USD 4.7 trillion in current prices – up from USD 4.5 trillion in 2023 and USD 4.2 trillion in 2022. This figure is nearly twice the combined total of the next most intangible-intensive economies: France, Germany, the UK and Japan (figure 11).

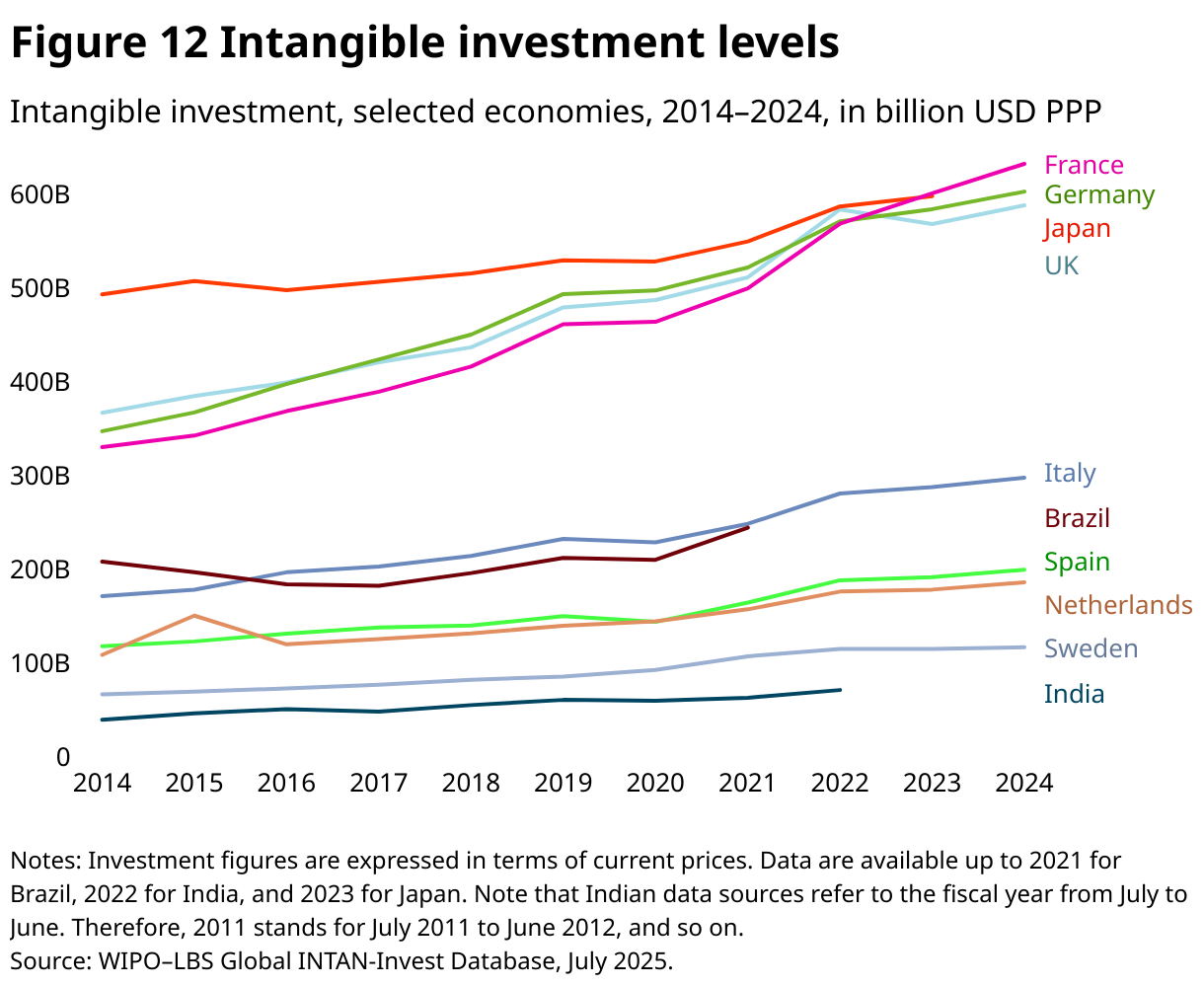

France has now surpassed both Germany and Japan – the long-standing leaders in intangibles – reaching over USD 631 billion of intangible investment in current prices in 2024, up by over 5 percent from USD 600 billion in 2023 (figure 12). In comparison, Germany’s intangible investment stood at USD 602 billion in 2024, while Japan’s latest available figure for 2023 was approximately USD 597 billion.

Between 2014–2024, Brazil and India recorded intangible investment levels comparable to several advanced EU economies. Brazil's intangible investment exceeds that of Spain, the Kingdom of the Netherlands and Sweden, reaching around USD 244 billion in 2021, while falling just short of Italy's level. India's intangible investment has grown steadily, reaching near USD 70 billion in 2022, compared to Sweden's USD 114 billion in the same year.

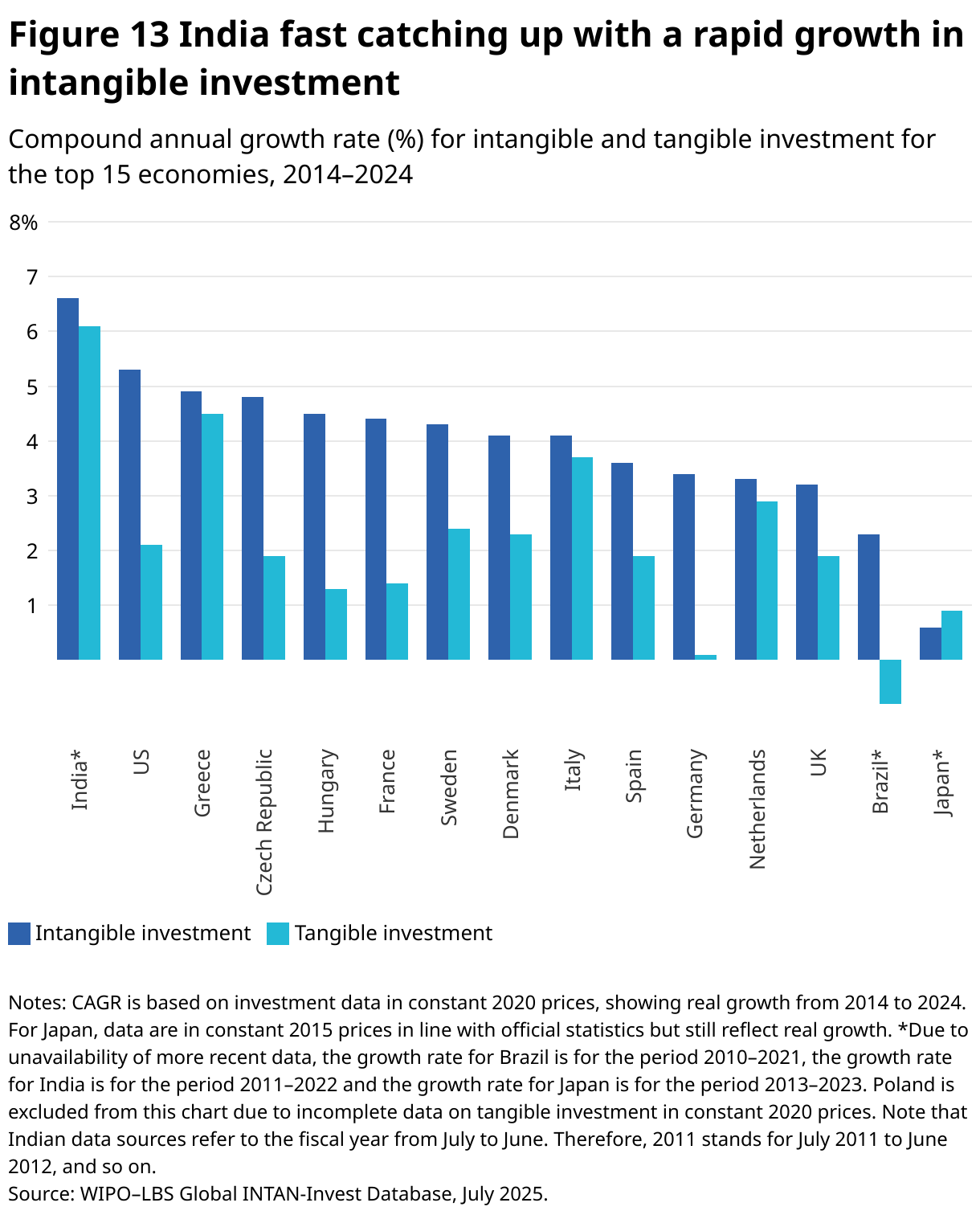

Stylized trend 5: India recorded the fastest growth in intangible investment between 2011–2022, outpacing the US, France and Sweden

India leads with the fastest intangible investment growth rates at nearly 7 percent annually between 2011–2022 (figure 13). This rapid growth may reflect India's ongoing catching-up process in building intangible capital from a relatively lower base.

Among the top 15 largest economies (by GDP in 2024), intangible investment generally grew faster than tangible investment between 2014–2024 (figure 13). India is followed by the US, with intangible investment growing by over 5 percent annually between 2014–2024. From 2013 to 2023, Japan's investment pattern favored tangible assets, growing at 0.9 percent versus 0.6 percent for intangibles. In stark contrast, major European economies (including France, Germany, Italy, Spain and the UK) saw a strong intangible investment growth at rates between 3–4.5 percent, well ahead of their tangible investment rates.

Brazil recorded an intangible investment annual growth rate of over 2 percent between 2010–2021, but its tangible investment declined by –0.8 percent over the same period.

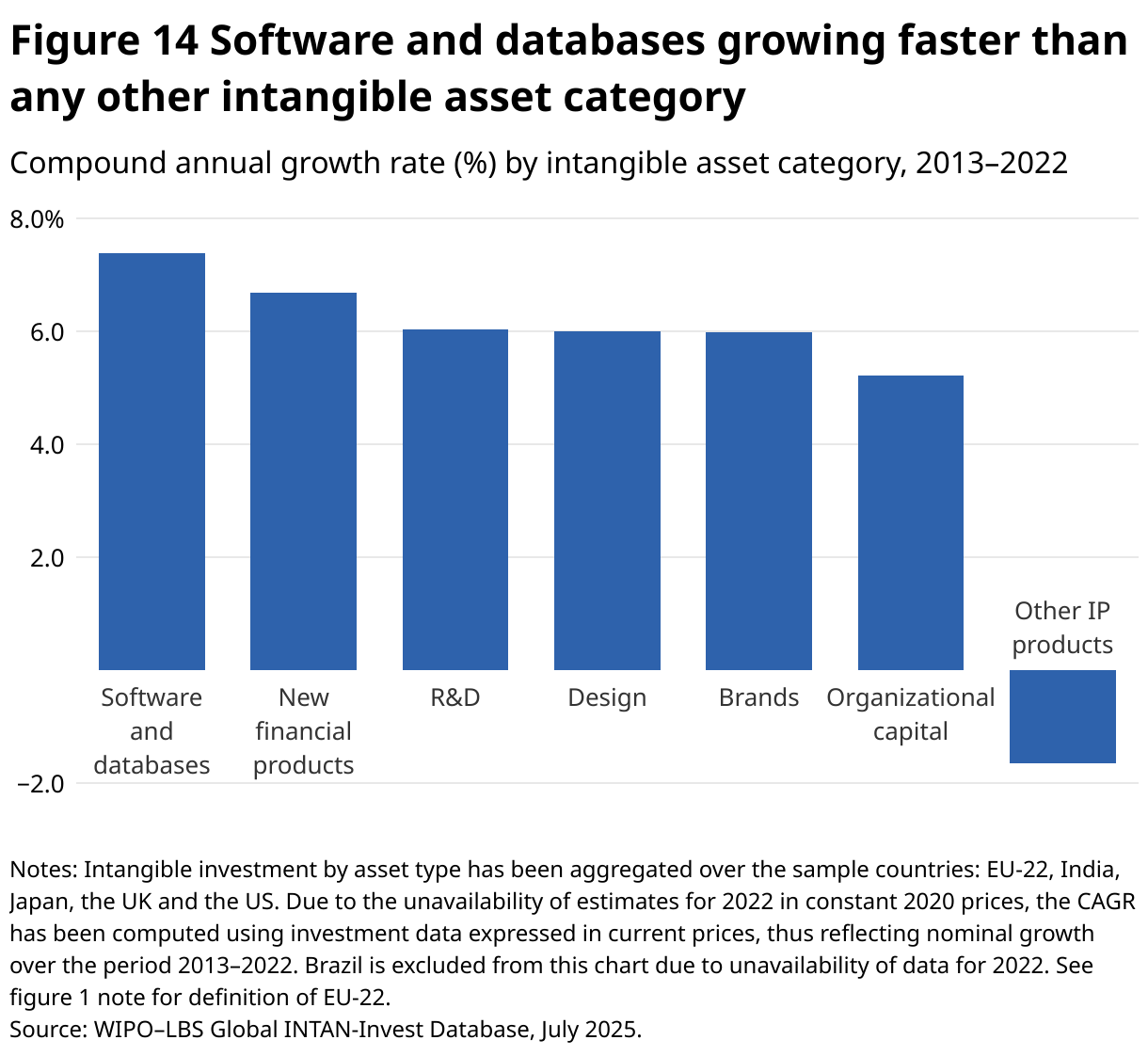

Stylized trend 6: Software and data make up the fastest growing category of intangible assets

Nominal growth data reveal software and databases to have been the fastest-growing intangible asset category over the period 2013–2022, expanding at above 7 percent annually (figure 14). This asset type is followed by new financial products (a relatively tiny component of intangibles), increasing at over 6 percent in nominal terms. Investment in R&D, design and brands has also experienced a relatively fast growth rate, each of these categories growing at around 6 percent per year.

Based on the latest available data, software and data grew over 9 percent in nominal terms between 2021–2022, well above the average growth rate over the 2013–2022 period. Notably, investment in brands and design has undergone a recent surge, with spending on brands rising by over 12 percent between 2021–2022, and design increasing by over 10 percent during the same period.

The growth in investment in software and data coincides with, and is likely driven by, the current artificial intelligence (AI) boom. Exploring this year’s Special theme – “What types of investments are driven by the AI boom?” – box 2 elaborates on the intangible and tangible investment components that are part of this AI boom. It presents a conceptual framework that distinguishes between AI-producing sectors (which create AI technologies) and AI-using sectors (which deploy AI across the broader economy). These two groupings reflect distinct waves of investment: an initial "capacity installation" phase focused on building AI infrastructure (e.g., micro-chips, data centers), and a longer-term "structural transformation" phase during which firms reconfigure business processes, develop new products and services, and retrain their workforces so as to embed AI more deeply. As AI reaches the stage of a general-purpose technology (GPT), its deployment drives broad-based intangible investment – particularly in data, software, skills and organizational capabilities – underpinning a fundamental transformation in how sectors like healthcare, education, manufacturing and energy both operate and generate value.

As box 2 highlights, tangible investment impacts from AI are already becoming apparent – especially in the US (see also Stylized trend 2). In 2023 and 2024, the US saw a notable tangible investment surge, fueled in part by large-scale spending on AI-related infrastructure by leading tech firms, including Amazon, Google, Microsoft, NVIDIA and OpenAI.

This US pattern is not yet global, however. AI infrastructure investment remains uneven across countries, with the US clearly out in the lead. For many other economies, tangible investment tied to AI is still at an early stage. The broader effects on national investment may only become apparent over the next one to four years.

AI allows computers and machines to simulate intelligence and problem-solving capabilities. To achieve this, AI has given rise to a unique investment pattern that explains the rapid growth in both tangible and intangible assets.

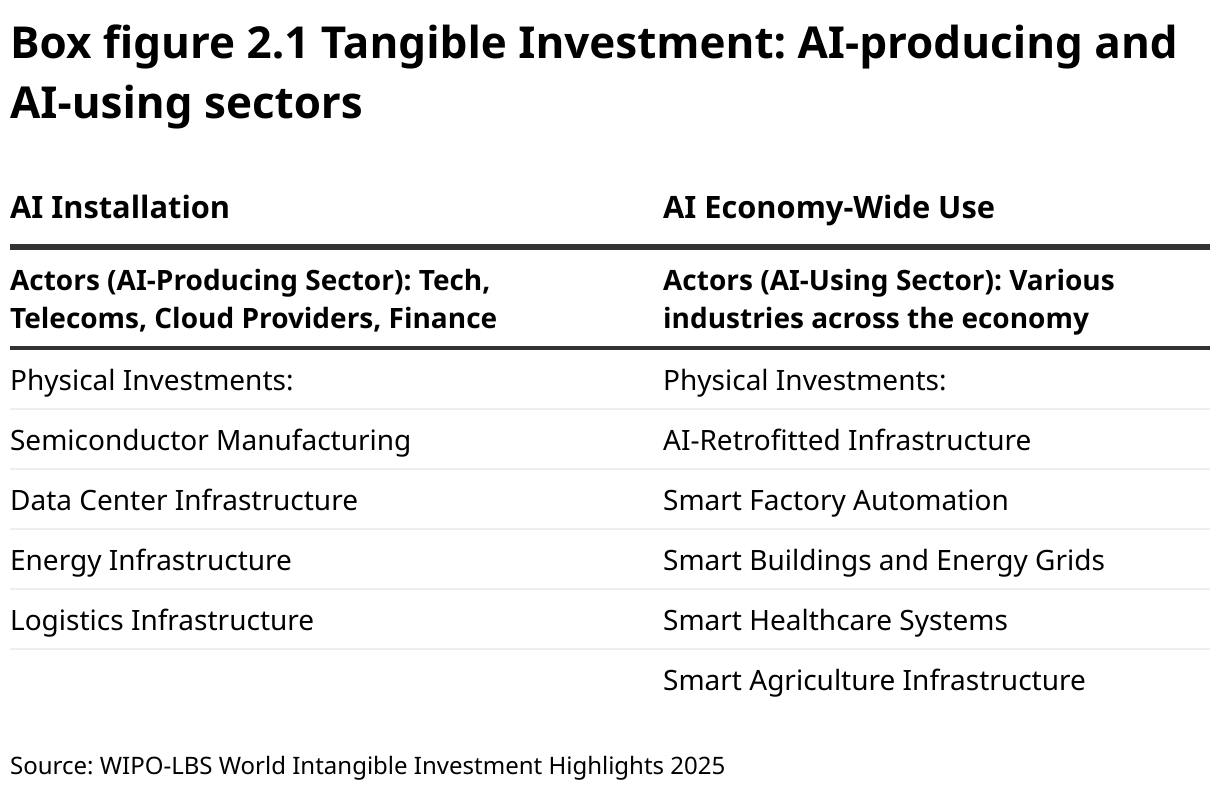

Specifically, AI drives two distinct investment waves: tangible assets for physical AI deployment and investments in three intangible asset groups, namely, digitized information, innovative property, and economic competencies (see annex figure A.2).

Tangible AI investment: building the physical foundation

AI deployment requires substantial physical investment that differs between AI-producing and AI-using sectors, and which follows a two-phase pattern: immediate capacity installation and longer-term structural transformation (see box figure 2.1).

AI-producing sectors, such as the aforementioned US-based companies, build technical foundations through hardware stack investments. Technology companies, cloud providers and infrastructure firms expand semiconductor manufacturing, construct data centers, address growing electricity demands and develop advanced logistics.

AI-using sectors deploy AI as a GPT throughout the economy. Infrastructure integrates smart sensors and edge computing. Factories install AI-integrated robots. Healthcare adopts AI-enabled imaging. Agriculture deploys precision irrigation and satellite analytics.

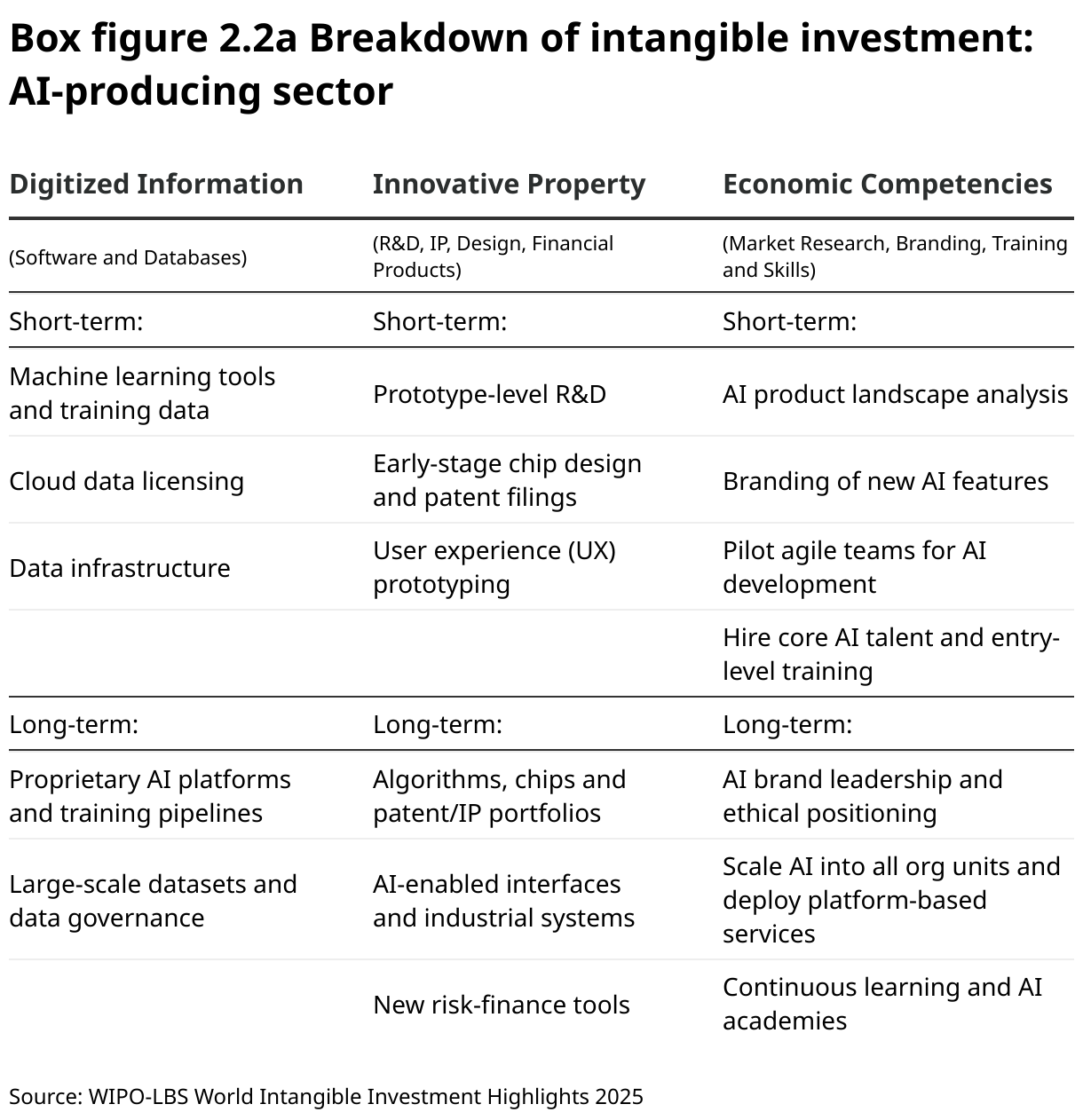

Intangible AI investment: the smart layer driving economy-wide impact

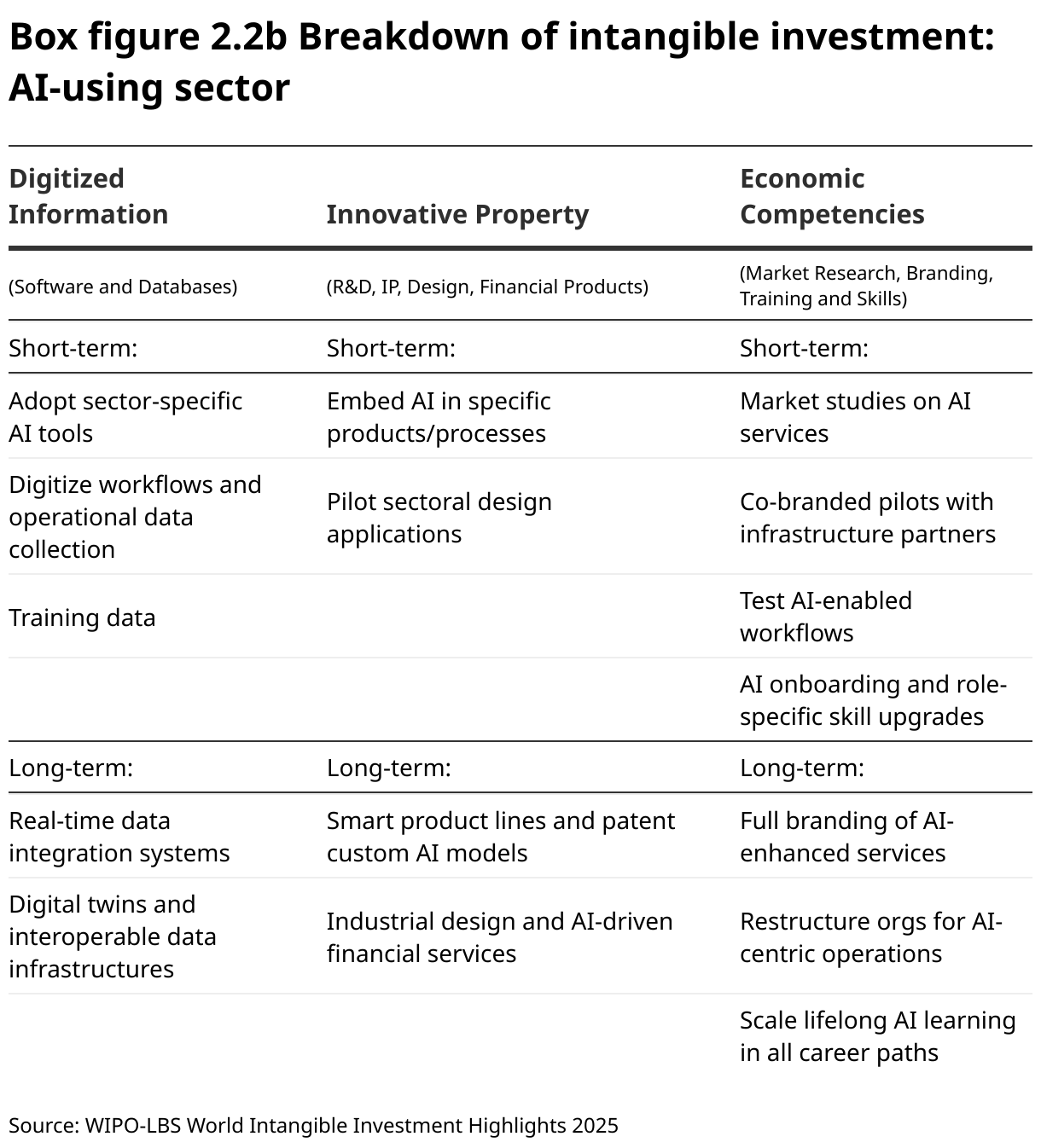

Subsequently, AI production and deployment depend equally on intangible investment across the three key intangible asset categories (box figures 2.2a and 2.2b):

Digitized information: Data serves as an essential AI input alongside computational software.

(8)See also WIPO’s Innovation Insights Blog (June 2025), Global software spending surges to close to USD 700 billion in 2024, up 50% from 2020; the United States extends its lead, available at www.wipo.int/en/web/global-innovation-index/w/blogs/2025/global-software-spending AI-producing firms invest in machine-learning tools, training datasets and proprietary platforms. AI-using sectors digitize operations and deploy sector-specific tools.Innovative property: AI-producing firms engage in prototype research, micro-chip design, and patent portfolio building. AI-using sectors embed AI into products and services, while protecting sector-specific know-how.

Economic competencies: AI drives investment into human capabilities and institutional transformation. AI producers and users both focus on talent development, process transformation and trust-building, while restructuring around AI-integrated workflows.

These intangible assets – data, IP, branding, workflows, and human capabilities – transform hardware into intelligent, trusted and productive systems. The combination of tangible infrastructure and intangible capabilities creates AI's economic impact, with investment patterns reflecting the technology's dual nature as both infrastructure and general purpose technology (GPT).

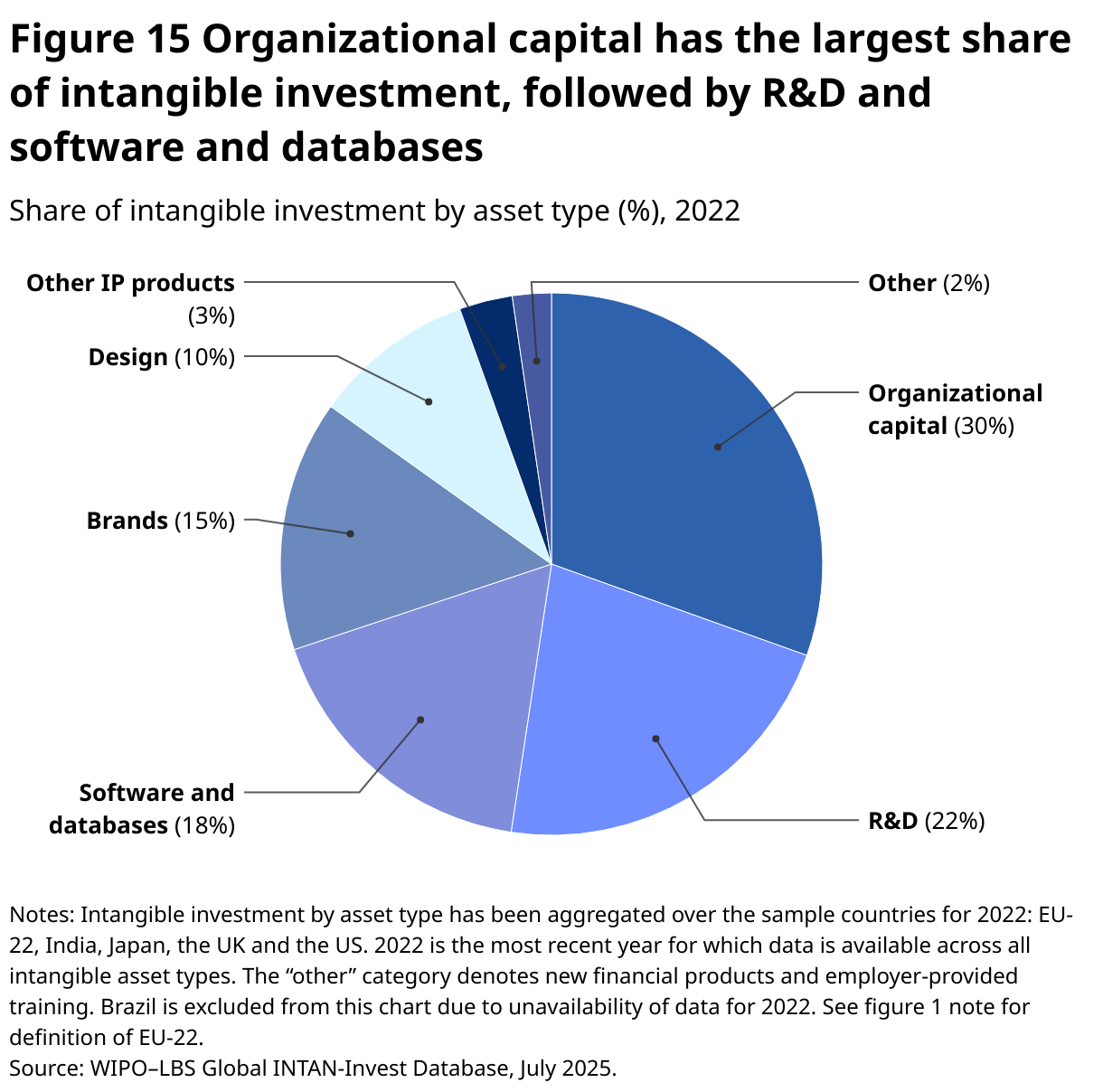

Stylized trend 7: Among intangible assets, organizational capital dominates, making up nearly one-third of total intangible investment in 2022

Organizational capital leads among intangible asset types, accounting for 30 percent of total intangible investment in 2022, up from 29 percent in 2021 (figure 15). Typically measured through a cost-based approach that considers a firm’s spending on organizational development, organizational capital refers to the internal know-how in managing and organizing a firm's operations. Strong internal processes and good management practices can help boost productivity and drive innovation within a firm, making organizational capital a valuable intangible asset.

Organizational capital is followed by R&D (22 percent, up from 19 percent in 2021), software and databases (18 percent, up from 16 percent), brands (15 percent, up from 14 percent) and design (10 percent, same as in 2021).

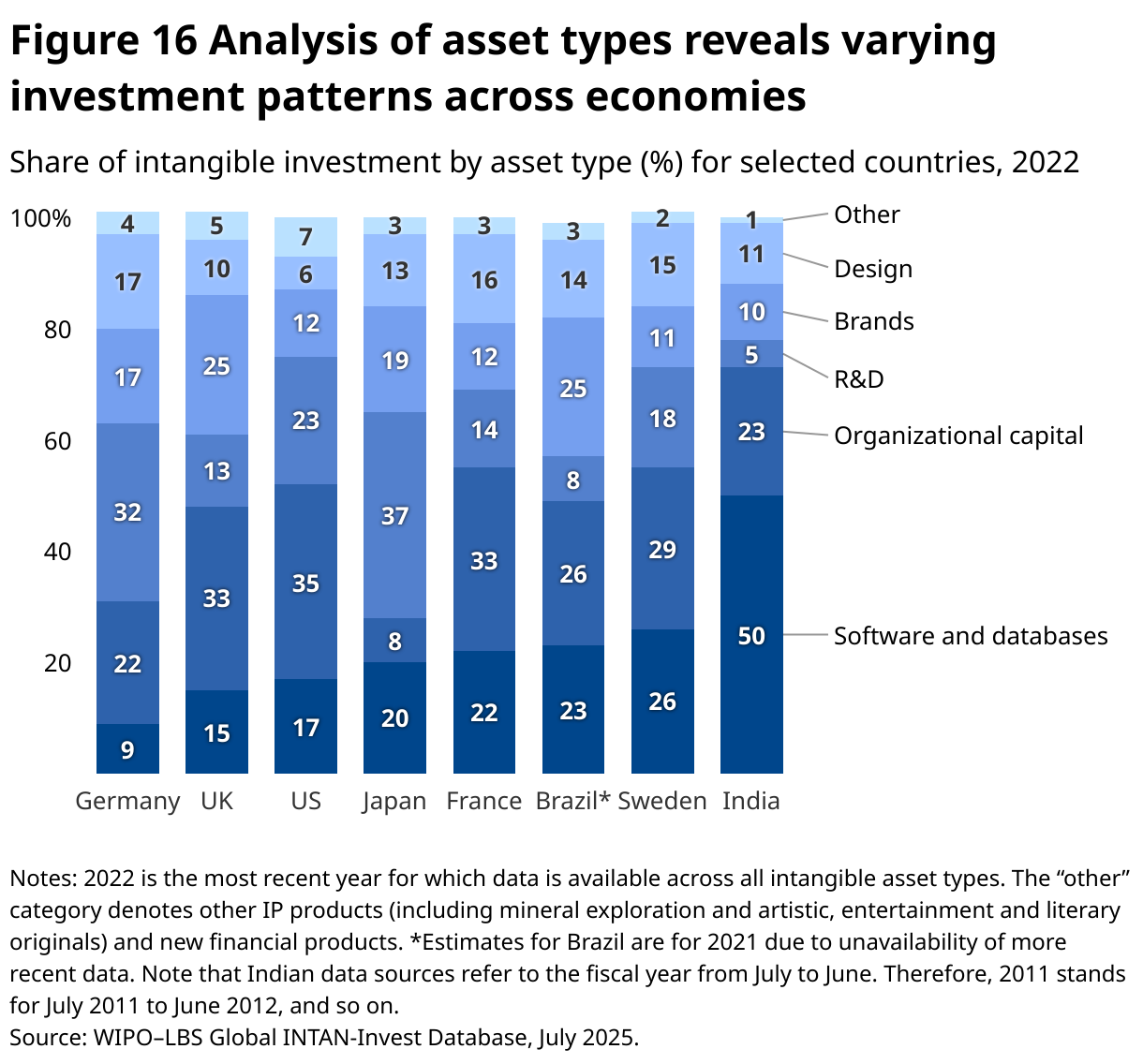

Country-specific patterns show notable differences in the composition of intangible investment (figure 16). India leads in software and databases, accounting for over 50 percent of its intangible investment – well above Sweden (26 percent), Brazil (23 percent) and France (22 percent). Japan and Germany stand out for having an emphasis on R&D (37 percent and 32 percent, respectively), consistent with their strong industrial base. The US invests most heavily in organizational capital (35 percent), while France and the UK also show large shares in this category (close to 33 percent for both). Brazil and the UK lead in brands, comprising close to 25 percent of total intangible investment for both, contrasting with India (10 percent) and the US (12 percent).

Annex: about the WIPO–LBS partnership on intangible assets in the global economy

Co-published by the World Intellectual Property Organization (WIPO) and Luiss Business School (LBS), the World Intangible Investment Highlights report serves as the key reference publication for global investment statistics in intangible assets from the Global INTAN-Invest Database.

Acknowledgements: The WIIH 2025 was prepared under the general direction of Daren Tang (Director General) in WIPO's IP and Innovation Ecosystems Sector led by Marco Alemán (Assistant Director General) and, more specifically, in the Department of Economics and Data Analytics led by Carsten Fink (Chief Economist). It was managed and drafted by Anmol Kaur Grewal (Fellow) and Sacha Wunsch-Vincent (Head, Section) and in collaboration with the LBS team, led by Cecilia Jona-Lasinio (Full Professor, LBS) with contributions from Filippo Bontadini, Carol Corrado, Jonathan Haskel, Massimiliano Iommi, Florencia Jaccoud, John Lourenze Poquiz and Patrick Serberis—all part of the Global INTAN-Invest team. The feedback of the Technical Advisory Board and the Steering Committee, in particular Bart van Ark (The Productivity Institute) on Box 2, as well as the participants of the 2025 Global INTAN-Invest Conference is thankfully acknowledged. Grateful thanks are extended for the support received in producing various country estimates. For Brazil, helpful contributions were provided by Leandro Veloso, Rodrigo Ventura (National Institute of Industrial Property), and Fernanda de Negri (formerly affiliated with the Institute for Applied Economic Research). For India, valuable support was received from Vivek Kumar Singh and Ashok Sonkusare (both NITI Aayog), Shrinivas Vijay Shirke (National Accounts Division, Ministry of Statistics and Programme Implementation), and Gaurav Thakur (Permanent Mission of India in Geneva). For Japan, contributions were made by Kyoji Fukao (Research Institute of Economy, Trade and Industry) and Tsutomu Miyagawa (Gakushuin University), and thanks are extended to Tomoki Sawai (WIPO Japan Office), as well as Takeshi Ueno and Maho Furuya (both Japan Intellectual Property Association). Sincere thanks are extended to the China National Intellectual Property Administration (CNIPA) and National Bureau of Statistics (NBS) for their helpful contributions and collaboration towards the potential inclusion of the People's Republic of China in future editions of this report.

Partnerships: This partnership includes participation from the African Union Development Agency (AUDA-NEPAD), the European Investment Bank (EIB), the Inter-American Development Bank (IDB), the International Monetary Fund (IMF), the Organisation for Economic Co-operation and Development (OECD), the US Bureau of Economic Analysis and the World Bank as Steering Committee members.

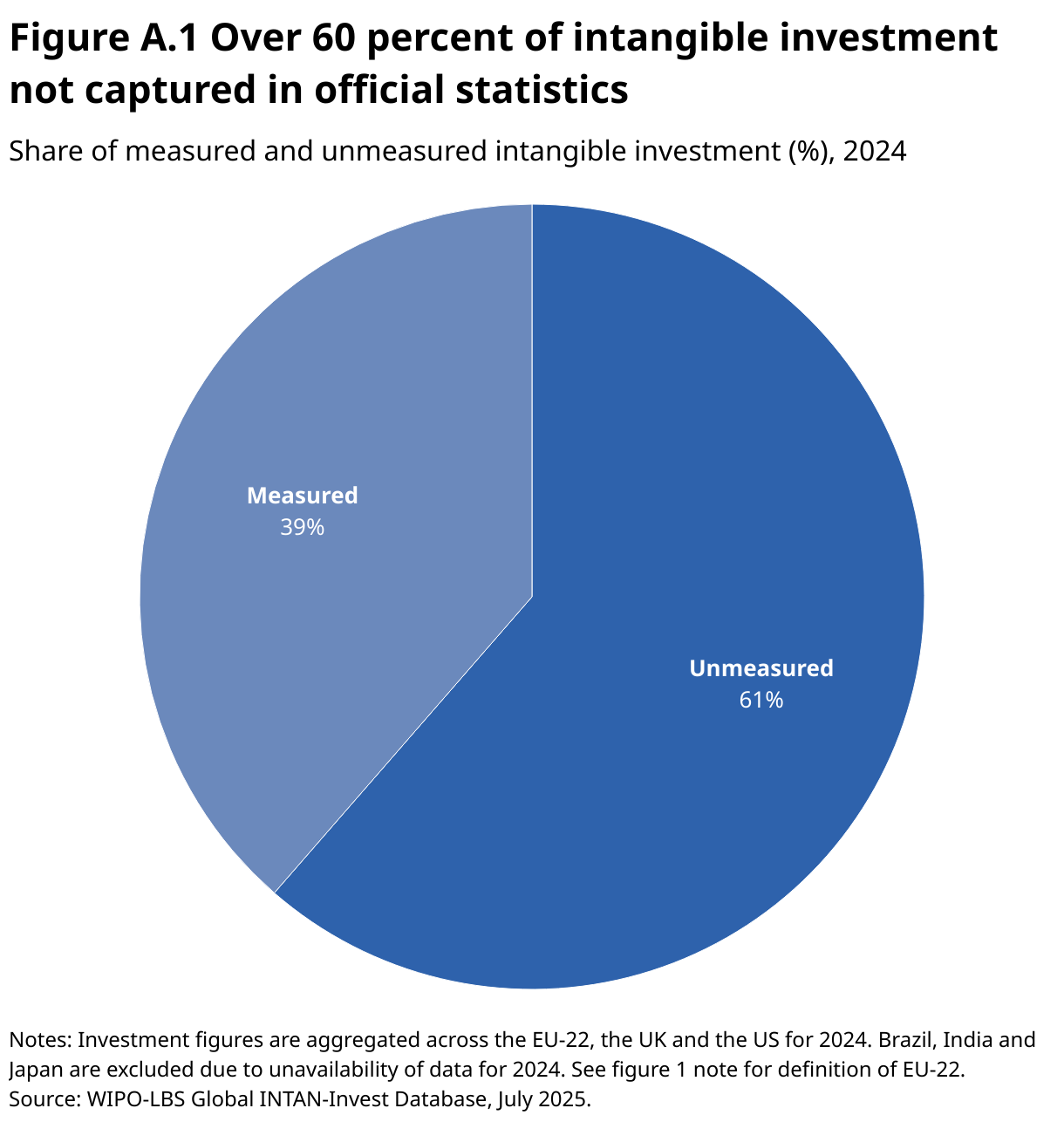

Measurement gaps: Despite the importance of intangible investment in driving innovation, productivity and economic growth, understanding of its size, composition and impact remains limited because of measurement constraints. The "non-physical" nature of intangible assets makes them intrinsically hard to measure and report. Many intangible asset types, such as brands or design, are not recognized as investment under national accounting frameworks, leading to over 60 percent of intangible asset investment remaining unmeasured (figure A.1). The WIPO-LBS Partnership seeks to address these measurement gaps by producing both annual and quarterly intangible investment estimates in a timely manner, with 2024 data available in July 2025. This project expands coverage beyond advanced economies to include emerging economies, starting with India.

Coverage: The latest July 2025 dataset release offers annual and quarterly estimates of intangible investment from 1995 to 2024 for 32 economies, including 27 EU economies, plus Brazil, India, Japan, the UK and the US. Due to differences in data availability, the asset coverage and time spans vary across economies. The analysis in this report covers those 27 countries (Brazil, EU-22, India, Japan, the UK and the US) with the most comprehensive asset and time coverage.

Measurement framework: The Global INTAN-Invest Database follows the national accounts framework proposed by Corrado, Hulten, and Sichel (2005, 2009), covering both unmeasured and measured intangible assets (figure A.2).